So, you’ve been searching for that perfect house to call a ‘home,’ and you’ve finally found it! The price is right, and in such a competitive market, you want to make sure that you make a great offer so that you can guarantee that your dream of making this house yours comes true!

Below are 4 steps provided by Freddie Mac to help buyers make offers, along with some additional information for your consideration:

1. Determine Your Price

“You’ve found the perfect home and you’re ready to buy. Now what? Your real estate agent will be by your side, helping you determine an offer price that is fair.”

Based on your agent’s experience and key considerations (like similar homes recently sold in the same neighborhood or the condition of the house and what you can afford), your agent will help you to determine the offer that you are going to present.

Getting pre-approved will not only show home-sellers that you are serious about buying, but it will also allow you to make your offer with confidence because you’ll know that you have already been approved for a mortgage in that amount.

2. Submit an Offer

“Once you’ve determined your price, your agent will draw up an offer, or purchase agreement, to submit to the seller’s real estate agent. This offer will include the purchase price and terms and conditions of the purchase.”

Talk with your agent to find out if there are any ways in which you can make your offer stand out in this competitive market! A licensed real estate agent who is active in the neighborhoods you are considering will be instrumental in helping you put in a solid offer.

3. Negotiate the Offer

“Oftentimes, the seller will counter the offer, typically asking for a higher purchase price or to adjust the closing date. In these cases, the seller’s agent will submit a counteroffer to your agent, detailing their desired changes, at this time, you can either accept the offer or decide if you want to counter.

Each time changes are made through a counteroffer, you or the seller have the option to accept, reject or counter it again. The contract is considered final when both parties sign the written offer.”

If your offer is approved, Freddie Mac urges you to “always get an independent home inspection, so you know the true condition of the home.” If the inspector uncovers undisclosed problems or issues, you can discuss any repairs that may need to be made with the seller or even cancel the contract altogether.

4. Act Fast

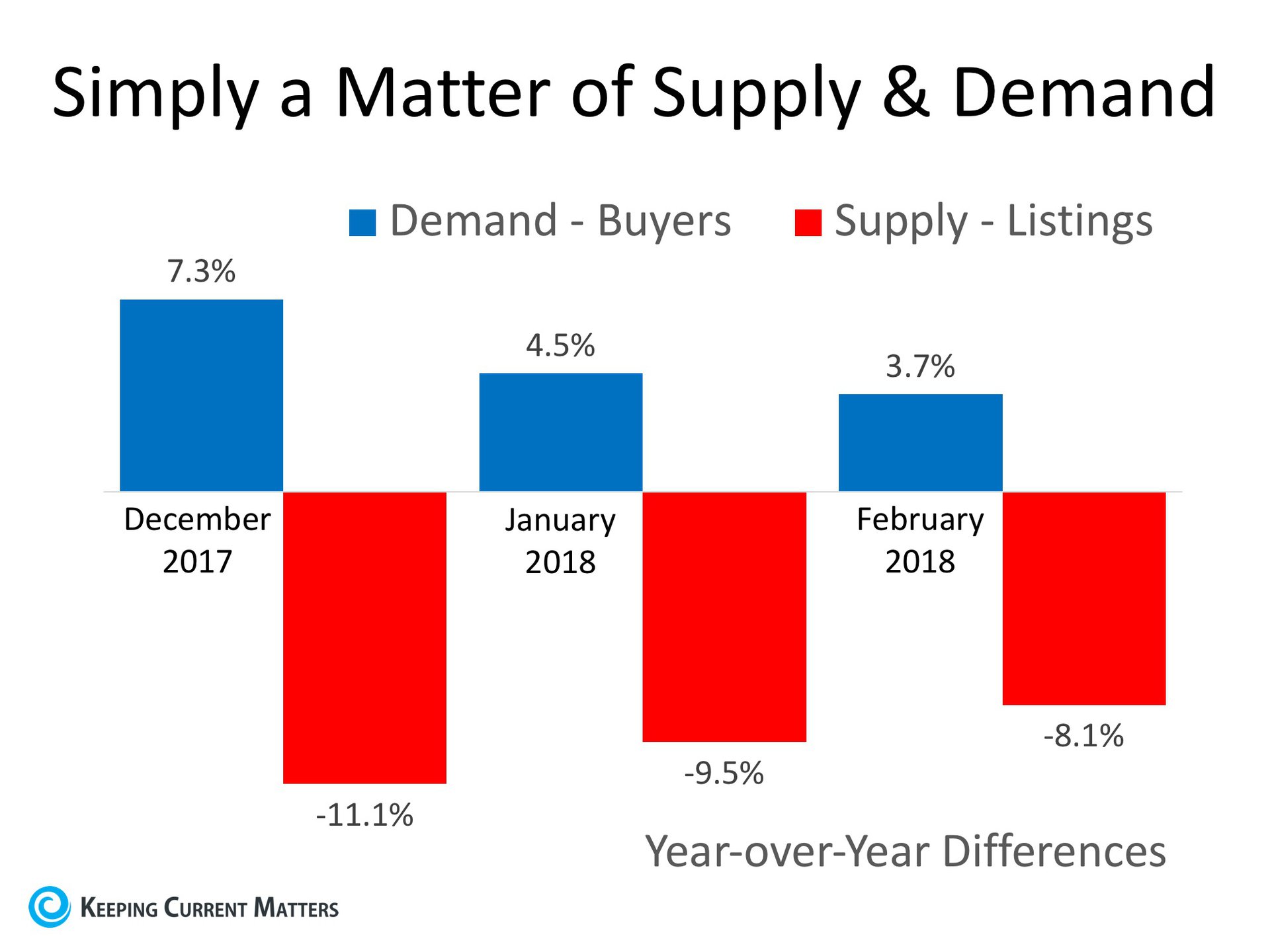

The inventory of homes listed for sale has remained well below the 6-month supply that is needed for a ‘normal’ market. Buyer demand has continued to outpace the supply of homes for sale, causing buyers to compete with each other for their dream homes.

Make sure that as soon as you decide that you want to make an offer, you work with your agent to present it as quickly as possible.

Bottom Line

Whether you’re buying your first home or your fifth, having a local professional on your side who is an expert in his or her market is your best bet in making sure the process goes smoothly. Happy house hunting!