View homes in the Dallas suburbs at NewAvenueRealty.com

Will the pandemic force people from the city to the sprawl of the burbs? Only time will tell but economists predict that they will.

While many people across the U.S. have traditionally enjoyed the perks of an urban lifestyle, some who live in more populated city limits today are beginning to rethink their current neighborhoods. Being in close proximity to everything from the grocery store to local entertainment is definitely a perk, especially if you can also walk to some of these hot spots and have a short commute to work. The trade-off, however, is that highly populated cities can lack access to open space, a yard, and other desirable features. These are the kinds of things you may miss when spending a lot of time at home. When it comes to social distancing, as we’ve experienced recently, the newest trend seems to be around re-evaluating a once-desired city lifestyle and trading it for suburban or rural living.

George Ratiu, Senior Economist at realtor.comnotes:

“With the re-opening of the economy scheduled to be cautious, the impact on consumer preferences will likely shift buying behavior…consumers are already looking for larger homes, bigger yards, access to the outdoors and more separation from neighbors. As we move into the recovery stage, these preferences will play an important role in the type of homes consumers will want to buy. They will also play a role in the coming discussions on zoning and urban planning. While higher density has been a hallmark of urban development over the past decade, the pandemic may lead to a re-thinking of space allocation.”

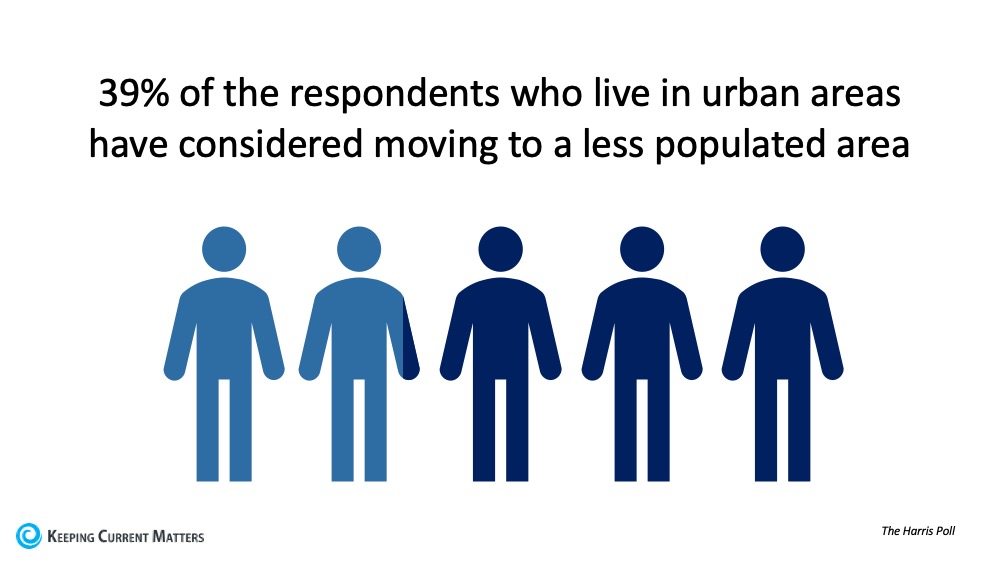

The Harris Poll recently surveyed 2,000 Americans, and 39% of the respondents who live in urban areas indicated the COVID-19 crisis has caused them to consider moving to a less populated area.Today, moving outside the city limits is also more feasible than ever, especially as Americans have quickly become more accustomed to – and more accepting of – remote work. According to the Pew Research Center, access to the Internet has increased significantly in rural and suburban areas, making working from home more accessible. The number of people working from home has also spiked considerably, even before the pandemic came into play this year.

Bottom Line

If you have a home in the suburbs or a rural area, you may see an increasing number of buyers looking for a property like yours. If you’re thinking of buying and don’t mind a commute to work for the well-being of your family, you may want to consider looking at homes for sale outside the city. Contact New Avenue Realty Group today to discuss the options available in your area.

In 2020, the property protest looks a tad bit different than it normally does. For starters, the assessments came out later than normal. There aren’t many in person protests (way I prefer) this year and most counties are asking people to protest online along with evidence. It is important to note the following when protesting in 2020: Any impact to market value due to factors during the 2020 calendar year would not impact appraised values until the following year.

Each year, respective counties send out new tax bills for the year to be paid by December. In Texas, one of the biggest expenses for homeowners are property taxes. We don’t have state income taxes therefore most local entities such as the county, school districts, county hospitals, cities, and sometimes county community colleges are paid through the property taxes.

The 2020 property tax assessments from various counties in the metroplex have been mailed out and guess what? Your property taxes may have increased. That’s the norm in Texas. What most people are seeing are a significant increase in their home value assessment (the property tax assessment value is getting really close to market values which we will talk more about later) by their counties. The key in protesting is to make sure you are being charged your fair amount in property taxes.

Did you know fewer than 20% of homeowners appeal their property taxes? This means they may pay more than their fair share. The best thing to do is to protest them. Why? You have a chance of lowering the amount you pay in property taxes by simply saying that this is too much. Let’s make a change in 2020 until the state government decides how they want to handle the property tax reform, shall we?

Here are tips to protesting your property tax assessment:

Make sure you have filed your homestead exemption.

You have until April 30th to file your homestead exemption with your county to save money on property taxes. You only have to do this once but if you failed to do it theJanuary – April AFTER you purchased your home, this is your chance to do it. A homestead exemption helps you save money on your property taxes. It also prevents your tax value from increasing more than 10% per year.

Check for mistake’s on the county’s description on your home.

Does the county have your 3 bedrooms, 2 bathrooms, formal dining home at 1805 square foot as 4 bedrooms and 3 bathrooms at 1925 square feet? It happens all the time and no one corrects it. A lot of county information is incorrect but we let it ride as gospel. Check your county’s website to make sure the square footage, number of bedrooms and bathrooms, and lot size are accurate in their assessment.

Gather Your Comps

It is important to keep up with the values of homes in your neighborhood. Most time people don’t realize what other homes are selling for. To gather more accurate comps, connect with a local REALTOR to see what homes have sold for within the last 3 months or 90 days in your neighborhood. In Denton County, Texas where I am located, the county has said they assessed the values based on the value on January 1, 2020. Therefore make sure the comps represent October 2019 to January 2020. Keep recent comps on you just in case.

You can enter your address below to determine what your home is worth.

Highlight Flaws in Your Home

Check high and low for the flaws.

We all love our homes and it is the best thing since slice bread. However, this is the time to really compare your home and get very judgmental about it. If you notice most of the homes that have sold nearby all have hardwood or some wood-like material, while you have carpet everywhere, take pictures of it. If you know your home is in need of a new roof or has foundation issues, take pictures and/or provide the quotes of those repairs that are needed.

Consider the negative influences near your nearby such as backing up to a busy street, water tower behind the home, or being on the main road to the neighborhood. Those are items that an appraiser would dock off your home’s market value when it is time for you to sell, use it to your benefit for your property taxes. P.S. I am not saying to trash your home or that you won’t ever be able to sell your home, this is to save money on your property taxes. I sold a home in Fort Worth last year and my clients ended up getting the property for less because the appraiser thought it was in a less desirable location than other homes comparable to it. It’s a gorgeous home and my clients love it. However, they got a win to buy it at a lesser price.

New Construction Woes

In most cases for newly built homes, there is a tricky line for homeowners. The previous year, your home was assessed based on land value. Now, it is based on the value of the home with a home on it. Check the price of the home that they county says your home is. Is it higher than what you paid for the home? Is it higher than what new homeowners can build the same exact home for? If your answer is yes to either one, that’s your protest. Texas is a non-disclosure state. In order to win the battle on the first one, you may have to show what you paid for your new home. The other option is to stop by the builder’s office (if they are still in the neighborhood) or pull it offline and see what your home is being sold for at base price. Is it lower than the county’s assessment? If so, your argument here is that your home has been lived in. No one is going to purchase your home for higher than what they can build their home for. Then take pictures of the things that you got standard (if you built) with the builder and haven’t updated.

Check Local Real Estate Trends

In addition to talking to your REALTOR for comps, ask them to pull the real estate trends. Homes have the potential to increase in value or appreciate. However, a property can decrease in value or depreciate. Is the price of homes sales decreasing in your zip code? A decrease in value can be caused in excess supply, lack of demand, deflation or other reasons that take away the property value. Home values fluctuate so don’t get nervous. It is just something for you to know and use in your protest. Homes appreciate normally 2-4% a year. Find out what is happening in your local area. It can be completely different from Aubrey to Crowley.

It can be that your area isn’t appreciating as much as the county THINKS it is appreciating.

Things to Remember

The county’s assessor’s don’t see the inside of your home. They can only see the outside of it. This is the time to show and prove what your home looks like. Use the knowledge that you have from the tips above to help lower your tax assessment value which in return lowers your property taxes. After you have your evidence, schedule an appointment with the county to present your case OR present the information online. It is important to protest annually to minimize your property taxes.

The counties are giving you 30 days from receipt to protest your online or through the mail. It is varying from county to county as some counties have yet to send out notices as of today. Find out how your local county tax assessor is handling property protest during COVID-19.

In uncertain times, there is hope and resources to make it through.

During the recent times of an outbreak that we haven’t experienced in our country, there are many people who are experiencing losses. New Avenue Realty is here to help guide those who will need assistance during this time. If your daily living has been affected in terms of income loss, here are options to get ahead of things.

Mortgagehelp needs

Contact your mortgage servicer (current company you pay your mortgage payments to) ASAP to know what options are. Below are a list of help currently being offered :

Fannie Mae Backed Loans

If coronavirus has caused job loss, income reduction, sickness, or other issues that impact your ability to make your monthly mortgage payment, relief options are available.

Homeowners impacted by this national emergency are eligible for a forbearance plan to reduce or suspend their mortgage payments for up to 12 months

Homeowners in a forbearance plan will not incur late fees

Credit bureau reporting of past due payments of borrowers in a forbearance plan as a result of hardships attributable to this national emergency is suspended

After forbearance, a servicer must work with the borrower on a permanent workout option to help maintain or reduce monthly payment amounts as necessary, including a loan modification

Foreclosure sales and evictions of borrowers are suspended for 60 days

Check to see if you have a Fannie Mae backed loan.

Freddie Mac is issuing a very similar policy during this time as well.

We are taking action to help make sure homeowners with Freddie Mac-owned mortgages who are directly or indirectly impacted by COVID–19 are able to stay in their homes during this challenging time. This includes offering the following mortgage relief options for those who are unable to make their mortgage payments due to a decline in income:

Providing mortgage forbearance for up to 12 months,

Waiving assessments of penalties and late fees,

Halting all foreclosure sales and evictions of borrowers living in Freddie Mac-owned homes until at least May 17, 2020,

Suspending reporting to credit bureaus of delinquency related to forbearance,

Offering loan modification options that lower payments or keep payments the same after the forbearance period.

Check to see if you have a Freddie Mac backed loan. There is help for those who have conventional borrowed loans for investment properties too. Your tenants may be affected and their late rent may cause a negative factor for your mortgage on the home.

FHA Backed Loans

If you have a FHA backed loan, the options above are geared more to conventional loan borrowers, here is information obtained on the HUD website to help assist:

The guidance issued today applies to homeowners with FHA-insured Title II Single Family forward and Home Equity Conversion (reverse) mortgages, and directs mortgage servicers to:

Halt all new foreclosure actions and suspend all foreclosure actions currently in process; and

Cease all evictions of persons from FHA-insured single-family properties.

“This is an uncertain time for many Americans, particularly those who could experience a loss of income. As such, we want to provide FHA borrower households with some immediate relief given the current circumstances,” said Federal Housing Commissioner Brian Montgomery. “Our actions today make it clear where the priority needs to be.”

FHA continues to encourage servicers to offer its suite of loss mitigation options to distressed borrowers – including those that could be impacted by the Coronavirus – to help prevent them from going into foreclosure. These include short and long-term forbearance options, mortgage modifications, and other mortgage payment relief options available based on the borrower’s individual circumstances.

Now is the time to be on the phones and contact your loan servicers if you’ve been affected by COVID-19. Check options to hold mortgage payments or even refinance your loan home. There are options and it is best to get ahead of it than to wait.

For refinance options, check out Keller Mortgage. Save on origination fees and even receive a $1000 credit on closing.

Nationwide banks are also stepping in to offer some assistance to waive fees for those affected by COVID-19. If you bank with a local bank as I do, check their website to see how they are helping those with financial difficulty during COVID-19 outbreak.

If you’ve had a loss of income and are suddenly unemployed, here is information from the State of Texas to help you during this time as well.

According to their website, If your employment has been affected by the coronavirus (COVID-19), apply for benefits either online at any time using Unemployment Benefits Services or by calling TWC’s Tele-Center at 800-939-6631 from 8 a.m.-6 p.m. Central Time Monday through Friday.

Renters

If you are currently renting an apartment or home, there are resources for you as well from the Texas Apartment Association.

Contact your property manager. The most important thing that you can do is communicate your situation with your Property Manager. Providing documentation from an employer or other documentation that shows how you have been impacted by this crisis will improve your chances for getting the help you need. Ignoring notices and requests to contact your Property Manager is not advised. Frequent and timely communication is the best course of action. The Texas Apartment Association has encouraged rental property owners to waive late fees and set up payment arrangements for residents impacted by the COVID-19 crisis. Please remember that they can’t help you if you do not communicate your situation with them. When court proceedings resume you will still owe any amounts due and may be subject to eviction; therefore, trying to work with your property to make payment arrangements is your best course of action.

Frisco ISD is offering WiFi drive up services for those who need access to Wifi at this time.

The District has installed additional wireless access points in 14 schools to expand the wifi signal to driveways and parking lots.

District-owned devices will automatically hook up to the “Frisco-ISD” wifi but personal devices can find “FriscoISD-Guest” as a new, expanded option. Students can reference this set of instructions for additional information or reach out to their campus digital learning coach.

This drive-up approach allows families to access wifi 24/7 from the comfort of their vehicle if their wireless should go out at home. The wireless can reach out to the front driveway of the campus, including that parking lot unless otherwise noted. Find locations on the website.

Meals

Local school districts are providing meals (some are even delivering them on bus routes to communities) to students Monday-Friday to help students and families with meals.

Prosper ISD food services will offer grab and go lunch pickup at Baker, Furr, Rucker, and Windsong Elementary campuses Monday – Friday from 11:00 am – 12:30pm beginning Wednesday, March 18th for the duration of the district facilities closure. Parents may drive through the front car loop to pick up meals from a staff member for their children. Please remain in your car if coming to pick up meals to help us continue the practice of social distancing. Meals will be provided in the same location for anyone walking up. In addition, many of our local community organizations have stepped up to provide food to those in need.

Here are a list of nearby food pantries in the North Texas too:

As Texans, we will make it through this pandemic. Here is the time to get to know what options we have and help a fellow neighbor or two. The pandemic is new to everyone and with everyone doing their part with stay at home orders, essential workers (praise to our healthcare workers and others) making sure we have some sort of normalcy. We will push through and in due time, this too shall pass.

If you have any questions or need more information on which direction to go, feel free to contact me at 972-813-9788 or [email protected]. If you know of an assistance program I can add to the list, email me to add to the list.

Texans can call 2-1-1 and select option 6 for questions about symptoms, travel concerns, unemployment insurance, emergency food assistance, city and state orders, and more.

Ever since I’ve finished my investment property, my Sundays have been freed to do some work at my personal home. Now with a shelter-in-place order from the counties in North Texas, I found myself completing home tasks. Prior to the quarantine orders, I figured we would be in so I went to purchase tools to do some projects.

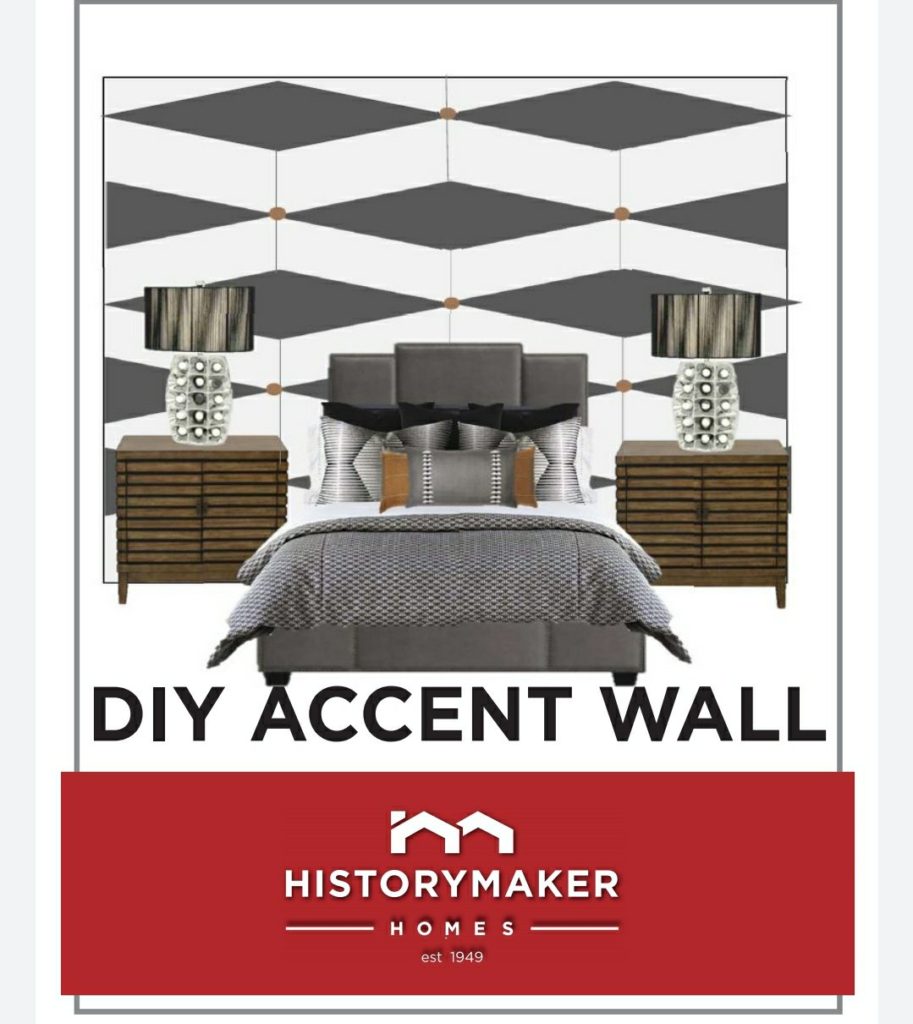

I’ve been wanting to redo my guest bedroom that I have coined “parents’ room”. It was my most dull room with no excitement. Well, my builder, HistoryMaker Homes, has an amazing DIY project gallery. I saw one or more that I loved and felt up to the challenge.

This is what I was hoping to achieve. The beginning. Change of heart. I was over it.

Then suddenly it hit me. I like to freestyle when doing things like this. Why not freestyle this wall with brush strokes? It is free form. No perfection (that was my problem with the designs) needed. Simple as simple can be.

I took one more direction from the HistoryMaker DIY gallery except for trim pieces, I have my paint brush.

This was my inspiration. I can do this. Simple.

That’s what I did and within no time, I had an accent wall in my guest bedroom.

This was very therapeutic in today’s time. I wanted something simple for this bedroom but not overwhelming. I love how simple this accent is. I may even add some art work above the bed.

As of now, the Texas governor hasn’t issued a lockdown for Texas. He is leaving it up to local officials. My county isn’t on lockdown but I’ve been working from home for a week now without going out much.

However, I’m sure I’ll have time to tackle a lot of projects.

Below are instructions for doing a brush stroke accent wall in your home. I’ve attached some other inspirations.

MATERIALS

Pint of Paint (I had a gallon because my original idea was to do a geometric accents)

Take some paper or small canva and test out brush strokes. I used the Sure Swatch to test different strokes for the look I wanted and decided which brush stroke I liked the most. I purchased four from The Home Depot. I ended up using the ALL 2″ Flat Brush. Check out more examples of this simple and easy project.

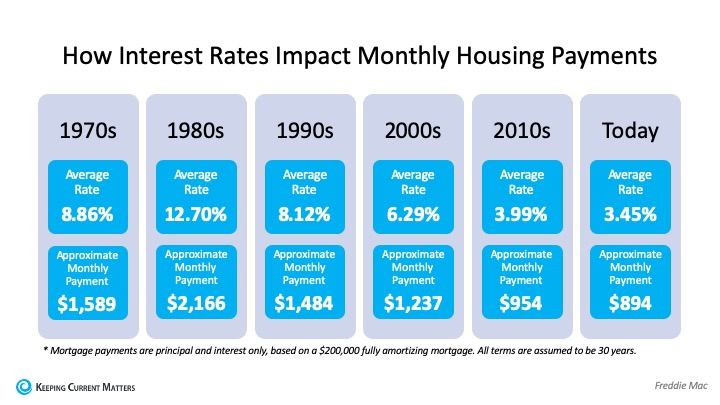

Spring is right around the corner, so flowers are starting to bloom, and many potential homebuyers are getting ready to step into the market. If you’re thinking of buying this season, here’s how mortgage interest rates are working in your favor.

“If you’re in the market to buy a home, today’s average mortgage rates are something to celebrate compared to almost any year since 1971…

Mortgage rates change frequently. Over the last 45 years, they have ranged from a high of 18.63% (1981) to a low of 3.31% (2012). While it’s not likely that the average 30-year fixed mortgage rate will return to its record low, the current average rate of 3.45% is pretty close — all to your advantage.”

To put this in perspective, the following chart from the same article shows how average mortgage rates by decade have impacted the approximate monthly payment of a $200,000 home over time:Clearly, when rates are low – like they are today – qualified buyers can benefit significantly over time.

Keep in mind, if interest rates go up, this can push many potential homebuyers out of the market. The National Association of Home Builders (NAHB) notes:

“Prospective home buyers are also adversely affected when interest rates rise. NAHB’s priced-out estimates show that, depending on the starting rate, a quarter-point increase in the rate of 3.75% on a 30-year fixed rate mortgage can price over 1.3 million U.S. households out of the market for the median-priced new home.”

Bottom Line

You certainly don’t want to be priced out of the market this year, and waiting may mean a significant change in your potential mortgage payment should rates start to rise. If your financial situation allows, now may be a great time to lock in at a low mortgage rate to benefit greatly over the lifetime of your loan.

Rates are low which is great for buyers who want more house without the extra payment OR who want the house without the extra interest. ??♀️ Everyone’s situation is different.

You know who else the rates are low are great for? Current homeowners. Seriously, as a homeowner, you have to stay on top on where you could be saving money. You can refinance your mortgage loan to save money on your principal and interest.

If you purchased a year or many moons ago, check your interest rates. Rates are hovering in the 3% range. This time last year, rates were in the mid 4s and December 2018/early January 2019, rates were in the 5%. What could you do with extra money in your pocket?

Do you have a good amount of equity because you purchased at least 3 years ago? Maybe instead of a rate and term refinance, you consider a cash out refinance? What could you do with X amount of money? Buy that investment property? Rent out your house and buy your next home to start building your portfolio. Pay bills. Etc.

Make it an annual thing to check where you could be saving money. Mortgage rates are low. Check for your savings for BUYERS AND CURRENT homeowners. If you need a list of lenders, send me a DM and I’ll connect you.

Congratulations! You just purchased your very first home. As you move from your apartment or rental home, you are trying to figure out how to really make this house a home.

Here are a list of trusted tools and products that I’ve used that I absolutely swear by to do some work around my house.

I’m a Home Depot fanatic as well as a #HomeDepotPartner. I’m can spend about as many hours here as I do HomeGoods and Target. Home Depot exclusively carries the Ryobi Tools line. These products are affordable and perfect for DIY projects for homeowners. I find myself in the power tool section just because.

This alone is more than enough for any homeowner doing basic work. I love the One Volt Line because you can use the same battery in soooo many products from Ryobi.

If you’re a money saving homeowner and like to do your own lawn unlike myself, then this leaf blower would come in extra handy. Spend less time raking and more time enjoy your free weekend.

A good water hose is needed. Listen, I opted for a $5 hose and let’s just say there was more water on me than the ground.

Paint Brushes

Touch up paint will be needed and you’ll want to be prepared.

Other items needed would be batteries, and light bulbs, and touch up paint! What are so other tools you feel homeowners should have? Let me know below ??!!!

This post contains affiliate links with Home Depot as a Home Depot Affiliate Partner.

Saving for a down payment is a key step in the homebuying process, and it’s not the only piece you need to include in your budget. Another factor that’s important to plan for is the closing costs required to obtain a mortgage.

“When you close on a home, a number of fees are due. They typically range from 2% to 5% of the total cost of the home,and can include title insurance, origination fees, underwriting fees, document preparation fees, and more.”

For those who buy a $250,000 home, for example, that amount could be between $5,000 and $12,500 in closing fees. Keep in mind, if you’re in the market for a home above this price range, your costs could be significantly greater. As mentioned before,

Closing costs are typically between 2% and 5% of your purchase price.

“There will be lots of paperwork in front of you on closing day, and not enough time to read them all. Work closely with your real estate agent, lender, and attorney, if you have one, to get all the documents you need ahead of time.

The most important thing to read is the closing disclosure, which shows your loan terms, final closing costs, and any outstanding fees. You’ll get this form about three days before closing since, once you (the borrower) sign it, there’s a three-day waiting period before you can sign the mortgage loan docs. If you have any questions about the numbers or what any of the mortgage terms mean, this is the time to ask—your real estate agent is a great resource for getting you all the answers you need.”

Bottom Line

Be sure your plan includes budgeting for what you need to purchase your dream home – without any surprises!

A considerable number of potential buyers shy away from the real estate market because they’re uncertain about the buying process – particularly when it comes to qualifying for a mortgage.

For many, the mortgage process can be scary, but it doesn’t have to be!

In order to qualify in today’s market, you’ll need adown payment (the average down payment on all loans last year was 5%, with many buyers putting down 3% or less), a stable income, and a good credit history.

Once you’re ready to apply, here are 5 easy steps Freddie Macsuggests to follow:

Find out your current credit history and credit score– Even if you don’t have perfect credit, you may already qualify for a loan. The average FICO Score® for all closed loans in September was 737, according to Ellie Mae.

Start gathering all of your documentation– This includes income verification (such as W-2 forms or tax returns), credit history, and assets (such as bank statements to verify your savings).

Contact a professional– Your real estate agent will be able to recommend a loan officer who can help you develop a spending plan, as well as help you determine how much home you can afford.

Consult with your lender– He or she will review your income, expenses, and financial goals in order to determine the type and amount of mortgage you qualify for.

Talk to your lender about pre-approval– Apre-approvalletter provides an estimate of what you might be able to borrow (provided your financial status doesn’t change) and demonstrates to home sellers that you’re serious about buying.

Bottom Line

Do your research, reach out to professionals, stick to your budget, and be sure you’re ready to take on the financial responsibilities of becoming a homeowner.

Book an appointment with #NewAveRealty at atfowlerrealtor.appointy.com.

One of my favorite neighborhoods off the 380 Corridor in Denton County is the Arrowbrooke community. This outdoor centered neighborhood makes it easy to enjoy nature and meet neighbors out hiking, biking, hitting the trails, or fishing at one of the many fishing ponds in the neighborhood.The latest home available in the neighborhood gives you all of that just steps from your front door.Stunning Arrowbrooke Home in Aubrey with spectacular backyard views features 4 bedrooms, 3 bathrooms,2.5 car garage. This fairly new home has 1.5 stories that feature an open floor plan, separate study, bright windows, spacious bedrooms, & wood look tile floors. The kitchen comes equipped w granite countertops, stainless steel appliances & wooden cabinets with crown molding. The second-floor ventures into a private suite space with a Gameroom, spacious bedroom, a full bath. Entertain in style & enjoy nature w the extended patio & pond views in this outdoor living centered neighborhood. This home comes with the remaining 2 & 10-year builder warranties.View more on this home at bit.ly/2104BrokenArrow. Schedule an appointment to view at atfowlerrealtor.appointy.com.