In today’s market, inventory dominates depending on what your price point is. Below $220K in DFW and it can be a struggle to find something. This can often be frustrating to be a first-time homebuyer if you aren’t prepared. Here are five tips fromrealtor.com’sarticle,“How to Find Your Dream Home—Without Losing Your Mind.”

1. Get Pre-Approved for a Mortgage Before You Start Your Search

One way to show you’re serious about buying your dream home is to get pre-qualified orpre-approvedfor a mortgage. Even if you’re in a market that is not as competitive, understanding your budget will give you the confidence of knowing whether or not your dream home is within your reach. This will help you avoid the disappointment of falling in love with a home well outside your price range.

2. Know the Difference Between Your ‘Must-Haves’ and ‘Would-Like-To-Haves’

Do you really need that farmhouse sink in the kitchen to be happy with your home choice? Would a two-car garage be a convenience or a necessity? Before you start your search, list all the features of a home you would like.Qualifythem as ‘must-haves’, ‘should-haves’, or ‘absolute-wish list’ items. This will help you stay focused on what’s most important.

3. Research and Choose a Neighborhood Where You Want to Live

Every neighborhood has unique charm. Before you commit to a home based solely on the house itself, take a test-drive of the area. Make sure it meets your needs for “amenities, commute,school district, etc. and then spend a weekend exploring before you commit.”

4. Pick a House Style You Love and Stick to It

Evaluate your family’s needs and settle on a style of home that will best serve those needs. Just because you’ve narrowed your search to a zip code doesn’t mean you need to tour every listing in that vicinity. An example from the article says, “if you have several younger kids and don’t want your bedroom on a different level, steer clear of Cape Cod–style homes, which typically feature two or more bedrooms on the upper level and the master on the main.”

5. Document Your Home Visits

Once you start touring homes, the features of each individual home will start to blur together. The article suggests keeping your camera handy and making notes on the listing sheet to document what you love and don’t love about each property you visit.

Bottom Line

In a high-paced, competitive environment, any advantage you can give yourself will help you on your path to buying your dream home.

Start with a consultation with New Avenue Realty at atfowlerrealtor.appointy.com.

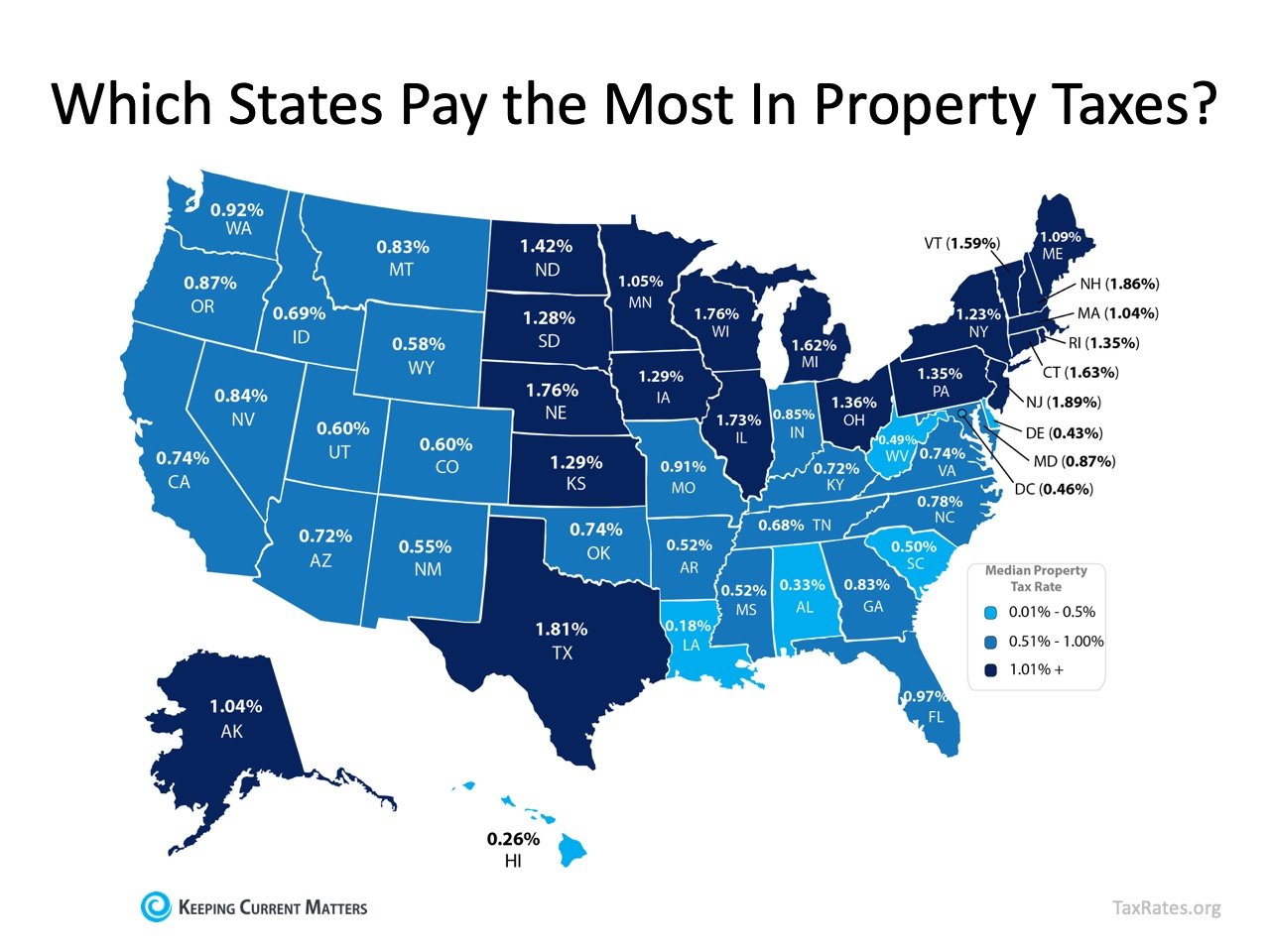

When buying a home, taxes are one of the expenses that can make a significant difference in your monthly payment. Do you know how much you might pay for property taxes in your state or local area?

When applying for a mortgage, you’ll see one of two acronyms in your paperwork –P&I or PITI– depending on how you’re including your taxes in your mortgage payment.

P&Istands forPrincipal and Interest, and both are parts of your monthly mortgage payment that go toward paying off the loan you borrow.PITIstands forPrincipal, Interest, Taxes, and Insurance,and they’re all important factors to calculate when you want to determine exactly what the cost of your new home will be.

“A municipal tax levied by counties, cities, or special tax districts on most types of real estate – including homes, businesses, and parcels of land. The amount of property tax owed depends on the appraised fair market value of the property, as determined by the property tax assessor.”

This organization also provides a map showing annual property taxes by state (including the District of Columbia), from lowest to highest, as a percentage of median home value.

The top 5 states with the highest median property taxes are New Jersey, New Hampshire, Texas, Nebraska, and Wisconsin. The states with the lowest median property taxes are Louisiana, Hawaii, Alabama, and Delaware, followed by the District of Columbia.

In Texas, we do not have states taxes which helps to pay for local services. Instead, the local municipalities are paid through property taxes. In your tax portion, you’ll notice taxing entities such as the city (“quasi city if you live in a MUD), county, school district, and any other county additions. For instance, Dallas County residents have Parkland Hospital and Dallas County Community College as additional tax entities.

Bottom Line

Depending on where you live, property taxes can have a big impact on your monthly payment. To make sure your estimated taxes will fall within your desired budget, chat with my real estate group at New Avenue Realty Group at Keller Williams today to find out how the neighborhood or area you choose can make a difference in your overall costs when buying a home.

Are you ready to buy a home and considering going in the route of new builds? It may seem like an easy enough process, where you get to call the shots of how you want your dream home to be, but there is a lot of risk when it comes to new construction if you are going in blindly. It’s unfortunately not as trouble free as we’d like to hope, if you don’t have the right representative by your side to help with the things that need to be looked out for from a professional’s eye. Below, we’ll dive into the many reasons you need a professional buyer’s agent representing you in the sale. They are, after all, on your side. And it’s their role to ensure you aren’t taken advantage of by the builders and their representatives in the transaction. 1. HIRING THE RIGHT BUILDER

The most important part of finding an agent is having a professional’s perspective to finding a builder with a great reputation. You get to benefit from your agent’s network of vendors, lenders, and home builders. They have the industry expertise to connect you with a builder that matches your needs, and more than likely, have already had experience with the builder with a past client. Or, if they haven’t worked with a builder you want to use directly, they can gather person-to-person recommendations from other agents to know the expected experience with said builder. They will help you find one, that not only delivers exactly what their clients want, but in a timely fashion.

2. THE RIGHT LOT IN THE RIGHT NEIGHBORHOOD

The lot you choose to go with in a new build can either be a positive to your new home, or detrimental. In the excitement of the process, we tend to overlook important features of a property. It’s important to have a professional to ensure you make a purchase that will best serve you. They’ll be able to find a neighborhood that best fits your lifestyle and a lot that has a location that works for you. Whether you’re single with pets, or a family with children, the lot location can really make a huge impact. Especially when it comes time to selling it in the future. These are important things your agent will be able to help walk you through, so your decisions work in your favor in the long term, as well as now.

3. UPGRADES AND PLAN MODIFICATIONS

Not only will your agent be able to ensure you get the upgrades and modifications that will best suit your lifestyle, but will also help you make decisions that will increase the value of your home in the long term. They are working for your best interest long term, and with an agent’s guidance, you can be sure to make changes that end up benefiting you.

4. HANDLING CONTRACTS AND PAPERWORK

Your agent will handle the contract and all of the paperwork, and they will be sure to review it to ensure that it is in your best interest. They will be able to help you break down the best loan types, purchasing processes, and steps to take that benefit YOU, not the builder. They are, after all, working for you. They’ll make sure there are no overlooked terms in a builder’s contract that could end up hurting you after you move in. Or even during the building process. You want to make sure you have a professional who is experienced with the paperwork and contracts and knows how to make revisions that work in a way that make you happy.

5. NEGOTIATIONS

It is imperative in the purchasing process to have an agent that is able to represent you and negotiate for you. The building process is so much more than having the builder put in your favorite counters and floors. They will be able to get you a price that actually benefits you – not the builder. They will be able to run a comparative market analysis to ensure you are paying a fair price for the property. You don’t want to end up overpaying for the home – it could put you in a tough spot when it comes time to sell. They’ll also be able to negotiate terms around building time frame, closings costs, and so many other aspects of a contract that you may otherwise overlook.

6. BUILDER’S AGENT REPRESENTS THEM, NOT YOU

It may seem easy just to pop into an office of a new build, or a builder’s office, and use the onsite agent. But keep in mind that this agent works FOR the builder, NOT for you. So they will be working to make sure the builder gets the best deal at the end of the day. By having a buyer’s agent of your own, you can ensure there is a professional on your side that can walk you through the process and avoid being taken advantage of during the transaction. They will also have a better handle on things when you hit bumps along the way. If you end up working with a builder who isn’t holding their end of the deal, they will have the power to make connections that ensure the builder holds their end of the contract terms.

1. I do not need to have the listing agent visit until my home is ready.

Wrong. In reality, the sooner the agent can get in, the better. Sellers, assuming the old rules still apply, might spend money on things that could harm a home’s potential and, conversely, fail to spend money where it matters.

Agentscan not only help sellersmaximize their potential, but they can also connect them with the trades and other professionals required to do it right.

2. I do not need to upgrade the property for sale.

Since increasing numbers of buyers are looking for move-in ready homes, the more a seller does toget the home to that level, the higher the returns. In an up market, sellers can reap a $2-$3 dollar return for every dollar spent.

In a declining market, they may not get 100 percent back, but they will get a sale. I frequently hear sellers ask, “Why should I upgrade? Won’t the new buyers come in and rip out all the stuff I just put in?”

That is not the right question. A better question is, “What can I do to make my online pictures sizzle to get the highest number of buyers through the front door regardless of what a buyer does once they own the home?”

If a seller can invest $1,000 on carpets and in the process make $3,000, does it matter what the new owner does once they move in?

3. I need open houses to sell my home.

The myth here is that buyers need to visit your home in person to decide whether they like it or not. In the new reality, buyers are visiting because they have already seen the home online and decided it was worth seeing in person.

Open housessimply make it easier for buyers who are already going to visit to actually get in. They also make it easy for the neighbors to come through — which is good because they frequently know someone looking to move into the area.

4. I need many open house signs at multiple key intersections.

Wrong again. Savvylisting agentsput out tons of signs because they are free advertising. Buyers who have seen the home online do not need directional signs to find the home. With open houses dates and times syndicating to all the major web portals, buyers simply use the GPS feature in their phones.

As for the neighbors, they will not come because you posted signs at far away intersections. To get them, you want signs close to the open house.

5. If buyers really want my house, they will pay more than market value.

Buyers are not running charities. Due to online AVMs (automated valuation models — thinkZestimate), buyers know when a property is overpriced and generally stay away, assuming the seller is unrealistic.

While pricing strategies vary from region to region, most agents know to recommend that sellers price listings close to market realities. As more listings come onto the market, buyers have more choices and migrate toward those they believe represent good values.

Sellers who insist they must net a specific amount, which in turn pushes the price too high, are only kidding themselves.

For sellers who have not sold a home in recent years, the new rules can be a shock. Ironically, since most sellers are also looking to buy a replacement home, all I usually have to do to change their thinking is to ask them how they are personally searching for homes in their new location.

They walk me through their process, and suddenly, in most cases, they get it.

Spend time getting to know your market and what TRULY sells NOT what you need to sell the home for. That stops the disappointments. You don’t want to end up chasing the market and sell your home for way less than expected. It can happen. Be prepared to price under market to move the property from the beginning.

Whether you’ve owned a home before, or you’re ready to jump into homeownership for the first time, there are always a lot of questions swirling around about what is truly required for a down payment, and how to best source down payment assistance. Let’s tackle these two today.

1. How much do you really need for a down payment?

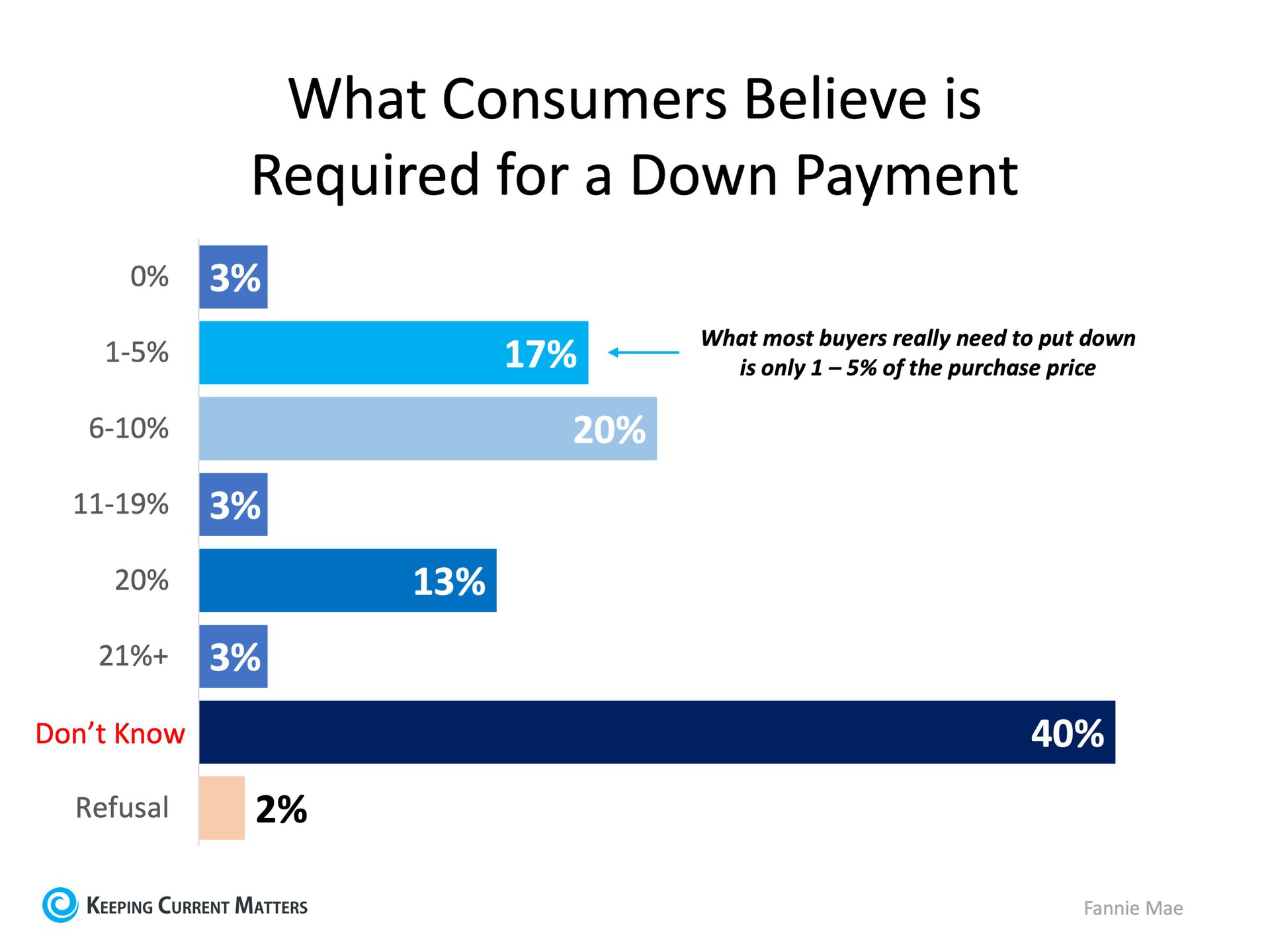

There is a long-standing misconception about down payment requirements. A survey from Fannie Maeshows only 17% of consumers know the minimum options are actually between 1 – 5% of the purchase price and 40% don’t know how much they need at all.There are many mortgage loans available that require as little as 3% down for first-time buyers, and some ask for only 3.5% down from repeat buyers. There are even loans available for Veterans that provide 0% down payment options too.

We’ve mentioned recently that you don’t need to come up with a 20% down payment to buy, and we’ve also shared how quickly you can save for a 3% or 10% down payment, depending on where you live. If you’re planning to put down just 3%, the research shows it may be possible in most states to have enough saved for a down payment in less than a year. That puts homeownership in a much closer reach for many potential buyers, maybe even you!

2. How can I get help with my down payment?

Regardless of the loans available, many buyers still need assistance with a down payment. The great news is, there are a lot of ways to tap into down payment assistance options. Here are just a couple of them:

Assistance from Family Members

The National Association of Realtors (NAR) said, “a third of recent first-time buyers received down payment assistance from family members.” They also mentioned, “the average net worth of those aged 75 and over stands at $264,800…They just might offer the boost the next generation needs to become homeowners.”

That means one of the ways to find help with a down payment is to accept a gift from a family member. If this is an option for you, make sure you talk to your loan officer before you accept the money, to ensure you document the process the way it is required by your loan. This way, it will be received properly and you can still potentially qualify.

Down Payment Assistance Programs

The reality is, not everyone has a loved one or a family member who can provide help with a down payment. There are, however, more than 2,500 down payment assistance programs available (by local areas like city, county, or neighborhood), and some of them are even specifically for first-time buyers.

The gap, as mentioned in the same survey, is “only 23% of consumers are familiar with low down payment programs.”

That’s why it is so important to get familiar with these options by doing your homework before you plan to buy a home. Determine what is available in the area where you ultimately want to live, so you have all the details you need to take advantage of the down payment assistance option that is best for your family.

Bottom Line

If buying a home is one of your long-term goals, you may be able to get there sooner than you think by tapping into one of the many down payment assistance programs available. Let’s connect you with one of my preferred lenders who specialize in these programs.

Chat with New Avenue Realty Group at 972-813-9788 or atfowler@kw.com.

Shifting trends and industry-leading research are pointing toward some valuable projections about the status of the housing market for the rest of the year.

If you’re thinking of buying or selling, or if you just want to know what experts are saying is on the horizon, here are the top three things to put on your radar as we head into the coming months:

Home prices are appreciating at a more normal rate: Home prices have been appreciating for about ten years now. Experts at theHome Price Expectation Survey, Mortgage Bankers Association, Freddie Mac,andFannie Maeare forecasting continuedgrowththroughout the next year, although it should be leveling-off to normal appreciation (3.6%), as we move into 2020.

Interest rates are low: Over the past 30 years, the average mortgage rate in the United States has been 8.27%, and rates even peaked as high as 18% in the 1980s. Today, at3.81%, the rate is considerably lower than the historical 30-year average. Although experts predict it may climb into the low 4% range in the near future, that’s still remarkably lower than our running average, suggesting a great time to get more for your money over the life of your loan.

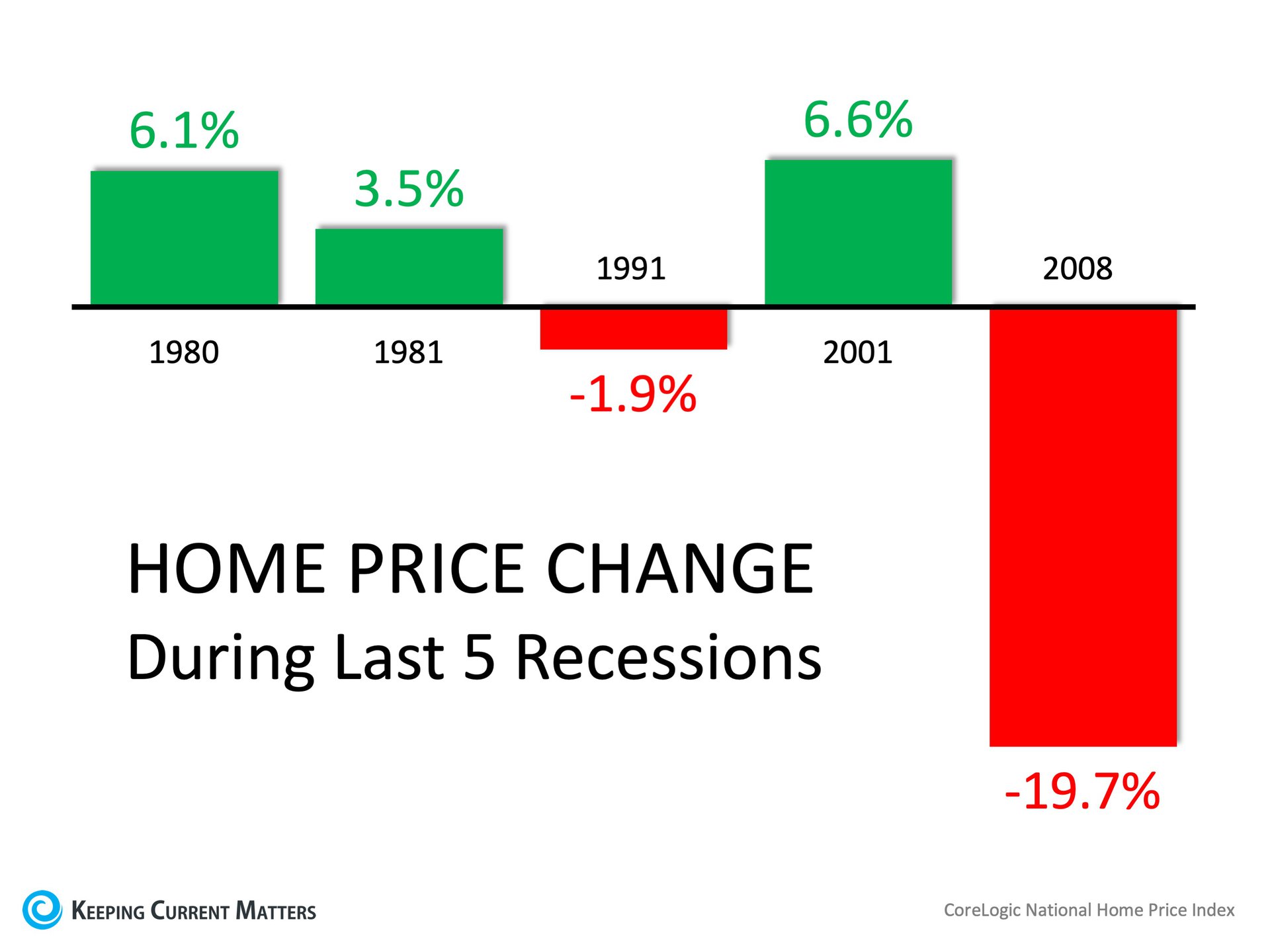

An impending recession doesnotmean there will be a housing crash: Although expert research studies such as those found in theDuke Survey of American CFOsand theNational Association of Business Economics, are pointing toward a recession beginning within the next 18 months, a potential recession isn’t expected to be driven by the housing industry. That means we likelywon’t experience a devastating housing crashlike the country felt in 2008. Expert financial analyst Morgan Houseltweeted:

“An interesting thing is the widespread assumption that the next recession will be as bad as 2008. Natural to think that way, but, statistically, highly unlikely. Could be over before you realized it began.”

In fact, during 3 of the 5 last U.S. recessions, housing prices actually appreciated:

Bottom Line

With prices appreciating and low interest rates available, it’s a perfect time to buy or sell a home. Reach out to New Avenue Realty Group of Keller Williams to see how you can take the next step in the exciting journey of homeownership.

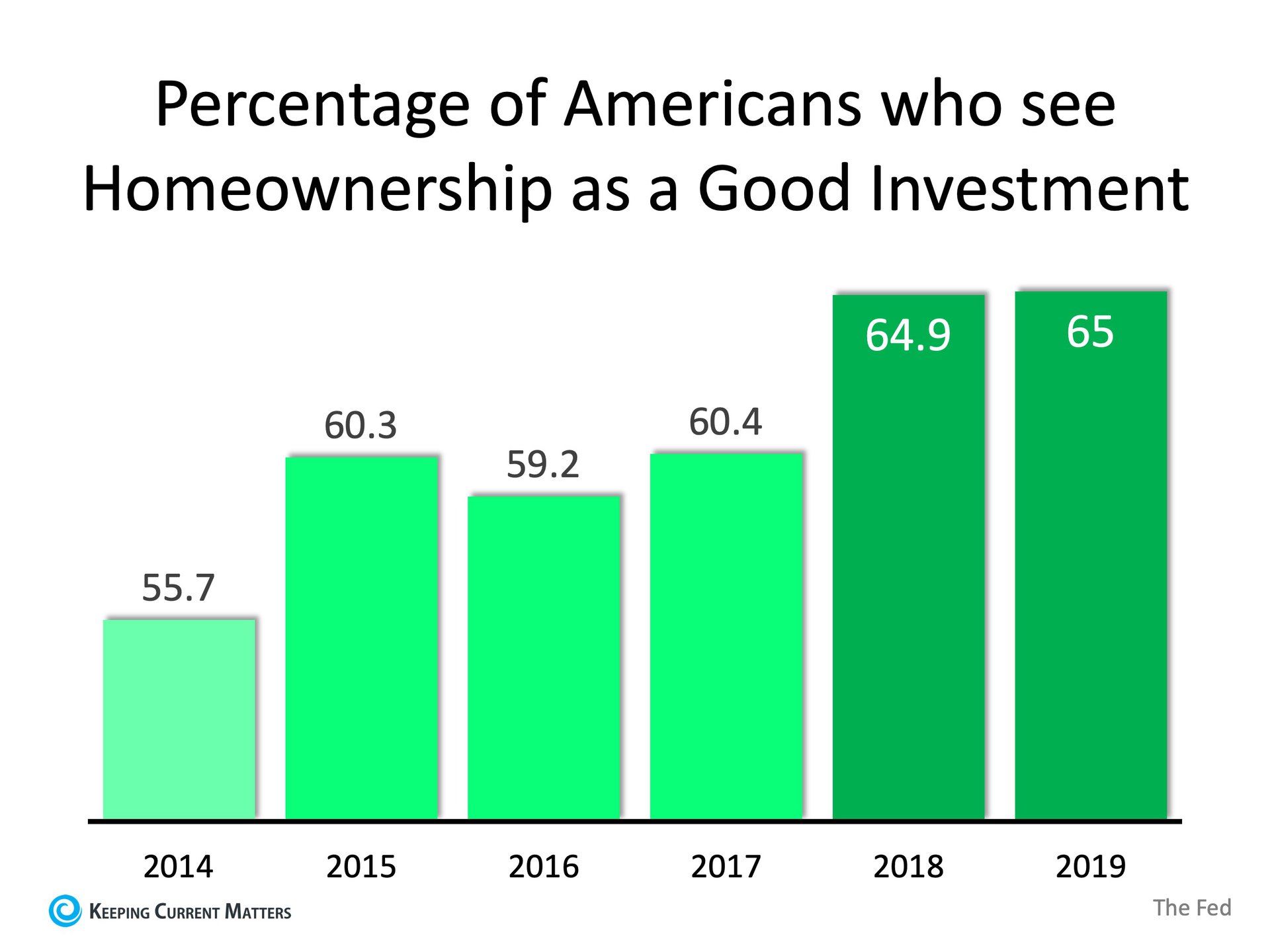

The Federal Reserve Bank(The Fed) recently released their2019 Survey of Consumer Expectations Housing Survey. The survey reported that 65% of Americans believe homeownership is a good financial investment. Since 2014, the percentage has increased by over nine percent.The Fed’s survey also showed that when the results are broken down by age, education, income, or region of the country, more than 55% of Americans in each category see homeownership as a good investment.

This coincides with a recentGallupsurveyof Americans which revealed that real estate was their number one choice for the best long-term investment when compared to stocks, savings accounts or gold.

Bottom Line

Americans’ belief in residential real estate as a good financial investment continues to grow as the housing market returns to normalcy.

It’s been almost two years since I’ve moved into my home and finally I have set my sights on completing my master bedroom. Since the beginning, I’ve said that this room would be my touch of gold. I started buying things that had gold in it. For the most part, I was happy with my bedroom.

Accenting my bedroom with gold pieces and using dark colors to bring out the contrasts. BEFORE

However, I needed a focal point. I thought about wallpaper. I bought this one roll from Target and just never got started. I thought about wood wall plank that got stuck to my wall with the samples. I felt defeated. I put the project on the backburner to flip homes instead.

It wasn’t until one day I was following Instagrammers, @angelarosehome and @philip_or_flop, that I discovered wainscoting. I was hooked and watching them tranform their homes as a DIY, I knew it was perfect for my bedroom. I actually did my first project at an investment property. It was super easy and fun. However, my master bedroom is 13 feet by 17 feet with 9 feet ceilings. I knew I wasn’t taking on that task by myself.

Hence a random night on Facebook marketplace, I discover Modern Wainscoting. It was the best thing ever and I was hooked. I followed the page AND found him on Instagram @modernwainscoting. I knew this would be my final decision maker on my master bedroom. Watch my bedroom transform and find details on items.

After painting the wall in Caviar by Sherwin Williams. Started with the borders then went to the middle. Created the rectangles in the inside. Accent Wall with Wainscoting is Complete.AFTER.

Accesories from Charter Furniture & At Home Stores. Lamp source listed below. Tufted Blue Stools – Tuesday Morning These may or may not be nightstands but I absolutely loved them. They have outlets and USB plugs on the back making them super useful.

Where do I like to shop for home furnishings? Target is one of my favorite places along with HomeGoods, At Home Stores, Tuesday Morning, and Wayfair for budget goods. You can even save 25% online when you shop at Target and pick up from the store. There are a few more items that I need to make this room complete (chandelier, chaise lounge, side board, wall decor). Follow me on Instagram to see more as I update my home.

Disclosure: The links in this post contain affiliate links and I will receive a small commission if you make a purchase after clicking on my link.

The time is here and you want to buy a home. There are so many people who are excited from moving from renter to homeowner throughout every year. However, with the Dallas-Fort Worth metroplex growing each and everyday, how do you decide on where to live?

For some people, the close proximity to work is important. For others, the close proximity to things outside of work is more important. I’ve actually had clients that had to live near Target. As a Target fanatic myself, I couldn’t blame them. After searching any and everywhere, they gave up the dream to buy a home near a Target. However, guess what? We found them a home in their price range ACROSS from a Target. LOOK AT GOD!

Now let’s talk a little more in depth on where to go. Many times we love where we rent or we hate it. Do you know the cost of homes where you live? Here is the chance to see where you can buy. One rule of thumb I tend to tell people is that you can either afford 2 times your monthly salary or four times your monthly salary. Why so? Well, when you purchase a home, a lender qualifies you based on your debt to income ratio.

Debt to Income Ratio

A debt-to-income, or DTI, ratio is derived by dividing your monthlydebt payments by your monthly gross income. The ratio is expressed as a percentage, and lenders use it to determine how well you manage monthly debts — and if you can afford to repay a loan.

Here’s a simple two-step formula for calculating your DTI ratio.

Add up all of your monthly debts. These payments may include:

Monthly mortgage or rent payment

Minimum credit card payments

Auto, student or personal loan payments

Monthly alimony or child support payments

Any other debt payments that show on your credit report

Divide the sum of your monthly debts by your monthly gross income (your take-home pay before taxes and other monthly deductions).

Convert the figure into a percentage and that is your DTI ratio.

Keep in mind that other monthly bills and financial obligations — utilities, groceries, insurance premiums, healthcare expenses, daycare, etc. — are not part of this calculation. Your lender isn’t going to factor these budget items into their decision on how much money to lend you. Keep in mind that just because you qualify for a $300,000 mortgage, that doesn’t mean you can actually afford the monthly payment that comes with it when considering your entire budget. – Excerpted from Bankrate.com

Your debt to income ratio (DTI) will determine which loan program makes sense for you as well. If you have a higher DTI, you may work best with a FHA loan as they have higher DTI qualifications up to 56.9%. If you are at 50% or below, you may qualify to do a conventional loan. If your DTI, exceeds any of these numbers, you may be asked to pay off some things to get where you need to be to get qualified.

Mortgages are NOT like rental qualifications. Rental qualifications are based on your monthly gross income being 3 times the monthly rent. A mortgage lender looks at ALL of your debt reported on your credit report. Let’s use an example for DTI qualifications.

EXAMPLE:

Gross Income – $48,000 salary = $4000 per month

Debt: Car Note – $350; Student Loans – $200, Credit Card 1 – $55; Credit Card 2 – $75; Personal Loan – $100. These are all based on monhtly payments NOT the overall payment. The total debt in this situation is $780/month. Now let’s say that the mortgage payment on said home would be $1800. That would bring your total monthly debt up to $2580. Would the lender qualify you for that home? Well, let’s see. Divide $2580/4000. That equals 65% of debt to income. Now, the lender may not qualify you for a home that would cost $1800/month. However, you may can get qualified for a home that cost $1450/month. Want to spend a little more? Your next option would be to eliminate some of the debt. In this example, to get the home that cost $1800, you’d need to eliminate $350 of debt. Where would that be from?

I tell clients that the way they could afford more house would be to either eliminate some debt, increase income, put down more money on the home, or all of the above.

Cost of Homes in DFW

As you can see, the average price of homes in DFW have increased 2.9% from May 2018 to May 2019 to $330,766. This isn’t to say that all homes in DFW are $330,766 but on average the home sales are.

How do you find which areas fit more of your budget? Consider the average sales prices of area. Let’s break it down within counties.

Some of the top places that my clients are moving to are the following: Aubrey, Forney/Heartland, Celina, and McKinney. Check out the prices of those areas below:

Buyer’s Market or Seller’s Market

The month’s of inventory determine whether we are in a buyer’s market or a seller’s market. If there is 6 months of more of inventory, we are in a buyer’s market. That means there is a home out there for at least two buyers. Homes aren’t scarce and the options are there. If we have less than 6 months of inventory, we are in a seller’s market. That means inventory is tight and you are more than likely to see multiple offers.

If we go back and compare those cities that we just looked at (Aubrey, Celina, McKinney, and Forney), you will see what type of market these areas are in. Each city will have different stats which is why it is best to get very specific on 3-4 areas.

If we look at DFW as a whole, you will see that the overall metroplex is still in a seller’s market with 3.4 months of inventory which is up 17.2% from May 2018.

This is just the basics of a buyer’s consultation with New Avenue Realty Group. We help clients get from curiosity to possibility. Let’s get you into your new avenue in the metroplex. Book an appointment with me at atfowlerrealtor.appointy.com.

When asked anything in real estate, I always like to give a list of pros and cons. As a Realtor, my job is to help you find the home that best fits what your needs are in the basis of the financial means that you have. We analyze those things based on a one-on-one conversation that we have from the consultation.

In a real estate market where home prices are rising, many have begun to reexamine the idea of buying a home, choosing instead, to rent for a while. But often, there is a dilemma: should you keep paying rent, knowing that rent is rising too, or should you lock in your housing cost and buy a home?

Let’s look at both scenarios and analyze the pros and cons of each:

Renting

With the housing market crash in 2008, many homeowners lost their homes and became renters. According to Iproperty Management, “the number of households renting their home … rose from 31.2% of households in 2006 to 36.6% in 2016”.

Some choose to rent because it is more convenient for their lifestyle. Those whose job requires frequent moves need the flexibility that a 6-12 month lease agreement gives them so they can move to their next assignment!

Many renters believe that renting is cheaper because they do not have to pay for maintenance and repairs. (Not true! Landlords work those expenses into your rent and other fees). Another reason many rent is that they feel like they cannot afford the down payment and closing costs required to buy a house, due to their inability to save much after paying their monthly expenses.

That can be true! Nearly 1 in 4 renters spend at least half their household income on rent. In 2017 the “severely” burdened renters’ rate was 24.7% with 24.9% reporting they were “moderately” burdened.

Renting also brings some financial disadvantages. Homeowners can take advantage of tax deductions that let them claim their property taxes and mortgage interest. Additionally, there is a big risk that your rent will go up every time you renew your lease, as we know the median asking rent has been increased steadily since 1988!

One of the major challenges with renting is that you don’t have a space to call your own. When you rent, you are paying your landlord’s mortgage, and therefore they are the beneficiaries of the equity gained from paying that mortgage.

Now let’s explore the other side: Homeownership

In the past, we have mentioned the many financial and non-financial benefits of becoming a homeowner. So, let’s just focus on the one big difference between renting and owning, the ability to lock in your housing cost!

Assuming you will have a fixed-rate mortgage, your costs are predictable! You will know exactly what your mortgage payment will be for the next 15-30 years. The homeownership rate in 2018 was 64.4%, and has been on the rise. Those households locked in their housing cost rather than wait for their landlord to raise their rent again!

What are the disadvantages of owning a home? Well, it is a long-term financial commitment! It is not easy to pack quickly and move. You will need time and good planning to do it in a short amount of time.

Unless you have a homeowner’s association (HOA) (and you pay an HOA fee) or a home warranty, you will be responsible for maintenance and taking care of the home. This may range anywhere from regular landscaping to major repairs.

Bottom Line

Like everything in life, there are pros and cons. What is better for you depends on your situation! If you are interested in becoming a homeowner and want to discuss the pros and cons, contact me at 972-813-9788 or atfowler@NewAvenueRealty.com so that I can help you review your current situation!

The Federal Reserve Bank

The Federal Reserve Bank