Every day, the world presents us with new technology. It seems like there isn’t much left that technology can’t do. Thankfully, with every advancement, many items have become more affordable.

While a high-tech home may not be the choice for everyone, there are plenty of budget-friendly options to try out if you are interested in making your home a little bit more accessible.

Here are 6 items to try:

Smart Speakers

Amazon Alexa

Setting reminders, asking questions, and playing music on demand has never been so easy! Smart speakers are capable of making lists for you, looking up recipes, and so much more. My favorite smart speaker is the Google Home mini. I keep one in the kitchen and one in my bathroom. Google is super helpful in finding my phone when I’ve lost it.

Smart Plugs

Left the coffee pot plugged in and need to turn it off, but you aren’t home? Smart plugs allow you to turn off (and on) something plugged in from your phone. These are also great for lighting systems like lamps or even holiday lights.

Smart Plug

Smart Doorbells

Smart doorbells are an incredible investment. Monitor who is ringing your doorbell, when packages are dropped off, and so much more all with your phone!

Smart Locks

Lost keys? Need to let someone in to water your plants while you are out of town? Smart Locks allow you to use your phone to lock and unlock your door, or just use a keypad!

Smart Switches

Smart switches allow you to turn lights off and on with your phone. Next time you forget to turn off the kitchen light and you are already in bed, smart switches can save the day!

Smart Bulbs

Adjust the brightness of color in any room when you install smart bulbs. Great for kids or rooms where you want to be able to dim the lights!

For my home, I have smart bulbs, smart door locks, smart garage opener, and smart doorbell. These are very essential for me as it helps me lock things from my phone and navigate my home while continuing to work.

Here is a bonus:

MySmart Q

This one was a lifesaver for me as it was my first time having a garage when I purchased my home. I no longer had to question myself on whether I closed the garage or not. If you have multiple garage bays, you can add on sensors to your bay.

Finding the right home to purchase today is one of the biggest challenges for potential buyers. With so few homes for sale and construction of newly built homes ramping up, you may be wondering if you should consider new construction in your search process. It’s a great question to ask, and one to look at from the pros and cons of what it means to buy a new home versus an existing one. Here are a few things to consider when making the best decision for your family.

New Construction

When buying a new home, you can often choose more energy-efficient options. New appliances, new windows, a new roof, etc. These can all help lower your energy costs, which can add up to significant savings over time. With programs like ENERGY STAR, your home also helps protect the environment and reduces your carbon footprint.

Lower maintenance that comes with a newer home is another great benefit. When you have a new home, you likely won’t have as many little repairs to tackle, like leaky faucets, shutters to paint, and other odd jobs around the house. With new construction, you’ll also have warranty options that may cover portions of your investment for the first few years.

Another solid benefit to new construction is customization. Do you want a mudroom, stainless steel appliances, granite countertops, hardwood floors, an office, or a multipurpose room to homeschool your children? These items can be customized to your specific needs during the design phase. With an existing home, you’re buying something that’s already completed, so if you want to make changes, you may need to hire a contractor to help get your home ready for your family.

Existing Home

When buying an existing home, you can negotiate with the current homeowner on price, which is something you generally don’t get to do with a builder. Builders know their material and construction costs, and they have a price set for the model you’re buying. So, if you want to negotiate, then maybe an existing home will be best.

For many families, having an established neighborhood is also important. Some buyers like to know the neighbors, if it’s family-friendly, and traffic patterns before making a commitment. When you buy new construction, you won’t have a full view of some of those details until the lots around you are sold.

Finally, timing comes into play. With an existing home, you can move in based on the timeline you agree to with the sellers. With new construction, you need to wait for the house to be built. Depending on the time of the year you’re buying and the region you’re in, the weather can also be a factor in the timeframe. This is something really important to keep in mind, especially if you need to move sooner rather than later. Over the past few months with COVID-19 and social distancing regulations, some areas for new construction have been delayed.

Bottom Line

Whether you want to buy a newly built home or one that’s already established, both are great options. They each have their pros and cons, and every family will have different circumstances driving their decision. If you have questions and want to know more about the options in your area, contact New Avenue Realty Group today so you can feel confident making a decision about your next home.

There’s great opportunity for today’s homeowners to sell their houses and make a move, yet due to the impact of the ongoing health crisis, some sellers are taking their time coming back to the market. According to Javier Vivas, Director of Economic Research at realtor.com:

“Sellers continue returning to the market at a cautious pace and further improvement could be constrained by lingering coronavirus concerns, economic uncertainty, and civil unrest.”

For homeowners who need a little nudge of motivation to get back in the game, it’s good to know that buyers are ready to purchase this season. After spending several months at home and re-evaluating what they truly want and need in their space, buyers are ready and they’re in the market now. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR) explains:

“A number of potential buyers noted stalled plans due to the pandemic and that has led to more urgency and a pent-up demand to buy…After being home for months on end – in a home they already wanted to leave – buyers are reminded how much their current home may lack certain desired features or amenities.”

The latest Market Recovery Survey from NAR shares some of the features and amenities buyers are looking for, especially since the health crisis has shifted many buyer priorities. The most common home features cited as increasingly important are home offices and space to accommodate family members new to the residence (See graph below):The survey results also show that among buyers who indicate they would now like to live in a different area due to COVID-19, 47% have an interest in purchasing in the suburbs, 39% cite rural areas, and 25% indicate a desire to be in small towns. As we can see, buyers are eager to find a new home, but there’s a big challenge in the market: a lack of homes available to purchase. Danielle Hale, Chief Economist at realtor.com explains:

“The realtor.com June Housing Trends Report showed that buyers still outnumber sellers which is causing the gap in time on market to shrink, prices to grow at a faster pace than pre-COVID, and the number of homes available for sale to decrease by more than last month. These trends play out similarly in the most recent week’s data with the change in time on market being most notable. In the most recent week homes sat on the market just 7 days longer than last year whereas the rest of June saw homes sit 2 weeks or more longer than last year.”

In essence, home sales are picking up speed and buyers are purchasing them at a faster rate than they’re coming to the market. Hale continues to say:

“The housing market has plenty of buyers who would benefit from a few more sellers. If the virus can be contained and home prices continue to grow, this may help bring sellers back to the housing market.”

Bottom Line

If you’re considering selling and your current house has some of the features today’s buyers are looking for, reach out to us at NewAvenueRealty.com. You’ll likely be able to sell at the best price, in the least amount of time, and will be able to take advantage of the low interest rates available right now when buying your new home.

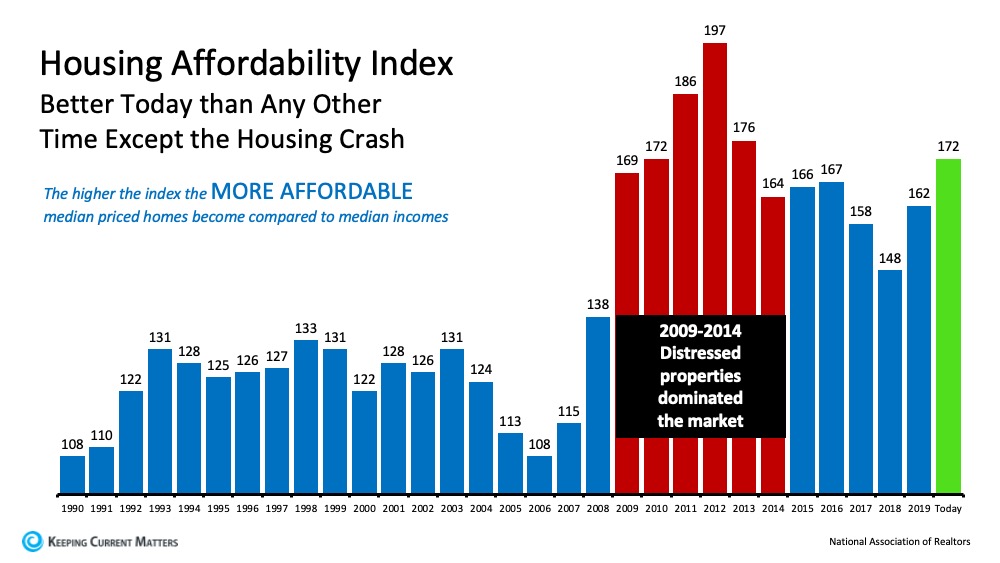

Everyone is ready to buy a home at different times in their lives, and despite the health crisis, today is no exception. Understanding how affordability works and the main market factors that impact it may help those who are ready to buy a home narrow down their optimal window of time to make a purchase.

There are three main factors that go into determining how affordable homes are for buyers:

Mortgage Rates

Mortgage Payments as a Percentage of Income

Home Prices

The National Association of Realtors (NAR), produces a Housing Affordability Index, which takes these three factors into account and determines an overall affordability score for housing. According to NAR, the index:

“…measures whether or not a typical family earns enough income to qualify for a mortgage loan on a typical home at the national and regional levels based on the most recent price and income data.”

Their methodology states:

“To interpret the indices, a value of 100 means that a family with the median income has exactly enough income to qualify for a mortgage on a median-priced home. An index above 100 signifies that family earning the median income has more than enough income to qualify for a mortgage loan on a median-priced home, assuming a 20 percent down payment.”

So, the higher the index, the more affordable it is to purchase a home. Here’s a graph of the index going back to 1990:The green bar represents today’s affordability. We can see that homes are more affordable now than they have been at any point since the housing crash when distressed properties (foreclosures and short sales) dominated the market. Those properties were sold at large discounts not seen before in the housing market.

Why are homes so affordable today?

Although there are three factors that drive the overall equation, the one that’s playing the largest part in today’s homebuying affordability is historically low mortgage rates. Based on this primary factor, we can see that it is more affordable to buy a home today than at any time in the last seven years.

If you’re considering purchasing your first home or moving up to the one you’ve always hoped for, it’s important to understand how affordability plays into the overall cost of your home. With that in mind, buying while mortgage rates are as low as they are now may save you quite a bit of money over the life of your home loan.

Bottom Line

If you feel ready to buy, purchasing a home this season may save you significantly over time based on historic affordability trends. Reach out to New Avenue Realty Group today to determine if now is the right time for you to make your move.

Lives have been changed greatly in 2020. Everything we have known prior to Marcg has been erased and we are in a new era.

I don’t know about you but there are things I’d like to stay long after we’ve dealt with the pandemic. Yes, let’s stay 6 feet from each other in public and to-go drinks (I’m free Louisiana so I was confused that I couldn’t get a Daiquiri to go when I moved to Texas).

Now what about the housing market? What has changed? Check out this replay of Buying a Home in 2020 and BEYOND!

Normally the hot seasons of the real estate market starts in the spring. More people tend to move in the summer months when school is out.

As far as Dallas/Fort Worth fairs, this was a week ago.

With stay-at-home orders starting to gradually lift throughout parts of the country, data indicates homebuyers are jumping back into the market. After many families put their plans on hold due to the COVID-19 pandemic, what we once called the busy spring real estate season is shifting into the summer. In 2020, summer is the new spring for real estate.

Joel Kan, Economist at The Mortgage Bankers Association (MBA) notes:

“Applications for home purchases continue to recover from April’s sizable drop and have now increased for five consecutive weeks…Government purchase applications, which include FHA, VA, and USDA loans, are now 5 percent higher than a year ago, which is an encouraging turnaround after the weakness seen over the past two months.”

Additionally, according to Google Trends, which scores search terms online, searches for real estate increased from 68 points the week of March 15th to 92 points last week. As we can see, more potential homebuyers are looking for homes virtually.

What’s the Opportunity for Buyers?

Another reason buyers are coming back to the market, even with forced unemployment and stay-at-home orders, is historically low mortgage rates. Sam Khater, Chief Economist at Freddie Mac indicates:

“For the fourth consecutive week, the 30-year fixed-rate mortgage has been below 3.30 percent, giving potential buyers a good reason to continue shopping even amid the pandemic…As states reopen, we’re seeing purchase demand improve remarkably fast, now essentially flat relative to a year ago.”

With mortgage rates at such low levels and states gradually beginning to reopen, there’s more incentive than ever to buy a home this summer.

What’s the Opportunity for Sellers?

Finding a home to buy, however, is still a challenge, as this spring sellers removed many listings from the market. Though more people are now putting their houses up for sale this month as compared to last month, current inventory is still well below last year’s level.

According to last week’s Weekly Economic and Housing Market Update from realtor.com:

“Weekly Housing Inventory showed continued tightening. New Listings declined 28% compared with a year ago, as sellers grappled with uncertainty and hesitated bringing homes to market. Total Listings dropped 20% YoY, a faster rate than in prior weeks, leaving very few homes available for sale. As Time on Market was 15 days slower YoY, asking prices moved up 1.5% YoY.”

If you’re thinking of selling your house this summer, now may be your best opportunity. With so few homes on the market for buyers to purchase, this season may be the time for your house to stand out from the crowd. Trusted real estate professionals can help you list safely and effectively, keeping your family’s needs top of mind. Buyers are looking, and your house may be at the top of their list.

Bottom Line

If you’re thinking of selling, many buyers may be eager to find a home just like yours. Reach out to me today to make sure you can get your house in on the action this summer. It is a seller’s market and a home with a pool is a ? commodity.

Will the pandemic force people from the city to the sprawl of the burbs? Only time will tell but economists predict that they will.

While many people across the U.S. have traditionally enjoyed the perks of an urban lifestyle, some who live in more populated city limits today are beginning to rethink their current neighborhoods. Being in close proximity to everything from the grocery store to local entertainment is definitely a perk, especially if you can also walk to some of these hot spots and have a short commute to work. The trade-off, however, is that highly populated cities can lack access to open space, a yard, and other desirable features. These are the kinds of things you may miss when spending a lot of time at home. When it comes to social distancing, as we’ve experienced recently, the newest trend seems to be around re-evaluating a once-desired city lifestyle and trading it for suburban or rural living.

George Ratiu, Senior Economist at realtor.comnotes:

“With the re-opening of the economy scheduled to be cautious, the impact on consumer preferences will likely shift buying behavior…consumers are already looking for larger homes, bigger yards, access to the outdoors and more separation from neighbors. As we move into the recovery stage, these preferences will play an important role in the type of homes consumers will want to buy. They will also play a role in the coming discussions on zoning and urban planning. While higher density has been a hallmark of urban development over the past decade, the pandemic may lead to a re-thinking of space allocation.”

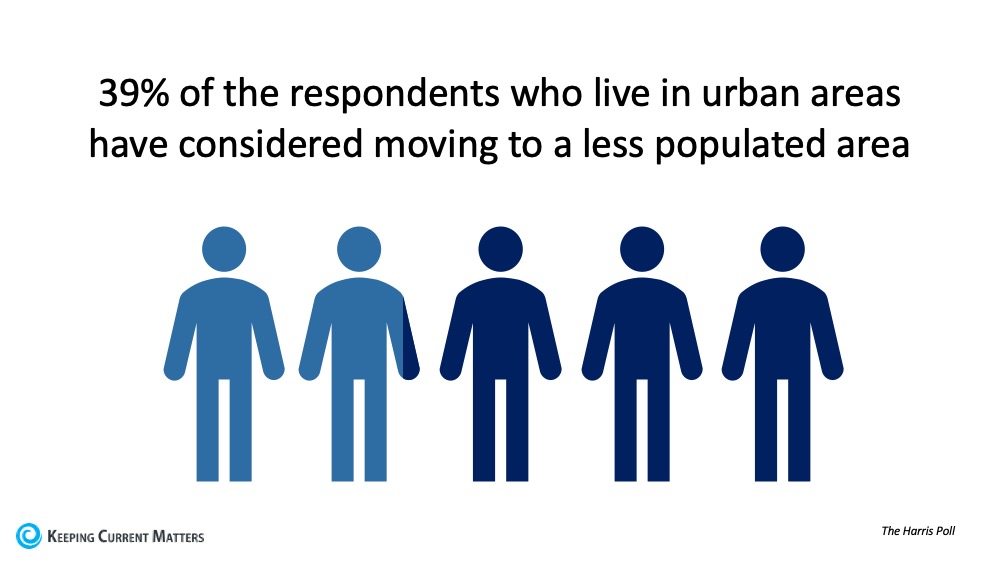

The Harris Poll recently surveyed 2,000 Americans, and 39% of the respondents who live in urban areas indicated the COVID-19 crisis has caused them to consider moving to a less populated area.Today, moving outside the city limits is also more feasible than ever, especially as Americans have quickly become more accustomed to – and more accepting of – remote work. According to the Pew Research Center, access to the Internet has increased significantly in rural and suburban areas, making working from home more accessible. The number of people working from home has also spiked considerably, even before the pandemic came into play this year.

Bottom Line

If you have a home in the suburbs or a rural area, you may see an increasing number of buyers looking for a property like yours. If you’re thinking of buying and don’t mind a commute to work for the well-being of your family, you may want to consider looking at homes for sale outside the city. Contact New Avenue Realty Group today to discuss the options available in your area.

View homes in the Dallas suburbs at NewAvenueRealty.com

Will the pandemic force people from the city to the sprawl of the burbs? Only time will tell but economists predict that they will.

While many people across the U.S. have traditionally enjoyed the perks of an urban lifestyle, some who live in more populated city limits today are beginning to rethink their current neighborhoods. Being in close proximity to everything from the grocery store to local entertainment is definitely a perk, especially if you can also walk to some of these hot spots and have a short commute to work. The trade-off, however, is that highly populated cities can lack access to open space, a yard, and other desirable features. These are the kinds of things you may miss when spending a lot of time at home. When it comes to social distancing, as we’ve experienced recently, the newest trend seems to be around re-evaluating a once-desired city lifestyle and trading it for suburban or rural living.

George Ratiu, Senior Economist at realtor.comnotes:

“With the re-opening of the economy scheduled to be cautious, the impact on consumer preferences will likely shift buying behavior…consumers are already looking for larger homes, bigger yards, access to the outdoors and more separation from neighbors. As we move into the recovery stage, these preferences will play an important role in the type of homes consumers will want to buy. They will also play a role in the coming discussions on zoning and urban planning. While higher density has been a hallmark of urban development over the past decade, the pandemic may lead to a re-thinking of space allocation.”

The Harris Poll recently surveyed 2,000 Americans, and 39% of the respondents who live in urban areas indicated the COVID-19 crisis has caused them to consider moving to a less populated area.Today, moving outside the city limits is also more feasible than ever, especially as Americans have quickly become more accustomed to – and more accepting of – remote work. According to the Pew Research Center, access to the Internet has increased significantly in rural and suburban areas, making working from home more accessible. The number of people working from home has also spiked considerably, even before the pandemic came into play this year.

Bottom Line

If you have a home in the suburbs or a rural area, you may see an increasing number of buyers looking for a property like yours. If you’re thinking of buying and don’t mind a commute to work for the well-being of your family, you may want to consider looking at homes for sale outside the city. Contact New Avenue Realty Group today to discuss the options available in your area.

In 2020, the property protest looks a tad bit different than it normally does. For starters, the assessments came out later than normal. There aren’t many in person protests (way I prefer) this year and most counties are asking people to protest online along with evidence. It is important to note the following when protesting in 2020: Any impact to market value due to factors during the 2020 calendar year would not impact appraised values until the following year.

Each year, respective counties send out new tax bills for the year to be paid by December. In Texas, one of the biggest expenses for homeowners are property taxes. We don’t have state income taxes therefore most local entities such as the county, school districts, county hospitals, cities, and sometimes county community colleges are paid through the property taxes.

The 2020 property tax assessments from various counties in the metroplex have been mailed out and guess what? Your property taxes may have increased. That’s the norm in Texas. What most people are seeing are a significant increase in their home value assessment (the property tax assessment value is getting really close to market values which we will talk more about later) by their counties. The key in protesting is to make sure you are being charged your fair amount in property taxes.

Did you know fewer than 20% of homeowners appeal their property taxes? This means they may pay more than their fair share. The best thing to do is to protest them. Why? You have a chance of lowering the amount you pay in property taxes by simply saying that this is too much. Let’s make a change in 2020 until the state government decides how they want to handle the property tax reform, shall we?

Here are tips to protesting your property tax assessment:

Make sure you have filed your homestead exemption.

You have until April 30th to file your homestead exemption with your county to save money on property taxes. You only have to do this once but if you failed to do it theJanuary – April AFTER you purchased your home, this is your chance to do it. A homestead exemption helps you save money on your property taxes. It also prevents your tax value from increasing more than 10% per year.

Check for mistake’s on the county’s description on your home.

Does the county have your 3 bedrooms, 2 bathrooms, formal dining home at 1805 square foot as 4 bedrooms and 3 bathrooms at 1925 square feet? It happens all the time and no one corrects it. A lot of county information is incorrect but we let it ride as gospel. Check your county’s website to make sure the square footage, number of bedrooms and bathrooms, and lot size are accurate in their assessment.

Gather Your Comps

It is important to keep up with the values of homes in your neighborhood. Most time people don’t realize what other homes are selling for. To gather more accurate comps, connect with a local REALTOR to see what homes have sold for within the last 3 months or 90 days in your neighborhood. In Denton County, Texas where I am located, the county has said they assessed the values based on the value on January 1, 2020. Therefore make sure the comps represent October 2019 to January 2020. Keep recent comps on you just in case.

You can enter your address below to determine what your home is worth.

Highlight Flaws in Your Home

Check high and low for the flaws.

We all love our homes and it is the best thing since slice bread. However, this is the time to really compare your home and get very judgmental about it. If you notice most of the homes that have sold nearby all have hardwood or some wood-like material, while you have carpet everywhere, take pictures of it. If you know your home is in need of a new roof or has foundation issues, take pictures and/or provide the quotes of those repairs that are needed.

Consider the negative influences near your nearby such as backing up to a busy street, water tower behind the home, or being on the main road to the neighborhood. Those are items that an appraiser would dock off your home’s market value when it is time for you to sell, use it to your benefit for your property taxes. P.S. I am not saying to trash your home or that you won’t ever be able to sell your home, this is to save money on your property taxes. I sold a home in Fort Worth last year and my clients ended up getting the property for less because the appraiser thought it was in a less desirable location than other homes comparable to it. It’s a gorgeous home and my clients love it. However, they got a win to buy it at a lesser price.

New Construction Woes

In most cases for newly built homes, there is a tricky line for homeowners. The previous year, your home was assessed based on land value. Now, it is based on the value of the home with a home on it. Check the price of the home that they county says your home is. Is it higher than what you paid for the home? Is it higher than what new homeowners can build the same exact home for? If your answer is yes to either one, that’s your protest. Texas is a non-disclosure state. In order to win the battle on the first one, you may have to show what you paid for your new home. The other option is to stop by the builder’s office (if they are still in the neighborhood) or pull it offline and see what your home is being sold for at base price. Is it lower than the county’s assessment? If so, your argument here is that your home has been lived in. No one is going to purchase your home for higher than what they can build their home for. Then take pictures of the things that you got standard (if you built) with the builder and haven’t updated.

Check Local Real Estate Trends

In addition to talking to your REALTOR for comps, ask them to pull the real estate trends. Homes have the potential to increase in value or appreciate. However, a property can decrease in value or depreciate. Is the price of homes sales decreasing in your zip code? A decrease in value can be caused in excess supply, lack of demand, deflation or other reasons that take away the property value. Home values fluctuate so don’t get nervous. It is just something for you to know and use in your protest. Homes appreciate normally 2-4% a year. Find out what is happening in your local area. It can be completely different from Aubrey to Crowley.

It can be that your area isn’t appreciating as much as the county THINKS it is appreciating.

Things to Remember

The county’s assessor’s don’t see the inside of your home. They can only see the outside of it. This is the time to show and prove what your home looks like. Use the knowledge that you have from the tips above to help lower your tax assessment value which in return lowers your property taxes. After you have your evidence, schedule an appointment with the county to present your case OR present the information online. It is important to protest annually to minimize your property taxes.

The counties are giving you 30 days from receipt to protest your online or through the mail. It is varying from county to county as some counties have yet to send out notices as of today. Find out how your local county tax assessor is handling property protest during COVID-19.

It’s been 2 year and 5 months since I’ve moved to my home. I’ve had projects on my list and just never found time until NOW. By the time the stay-at-home orders are lifted, I may have a whole new home. All that is missing is a spring update from HomeGoods.

The latest part of the DIY project is installing cabinet knobs to my kitchen cabinet. This isn’t the finale for my kitchen but a practice to see how to do this. ?

I’ll teach you and then send me a finished product of your kitchen or bathroom hardware install.

Here’s a video to show you how it is done. Products used are tagged below. The links in this post contain affiliate links and I will receive a small commission if you make a purchase after clicking on my link.

*Not shown in the video and thought I needed to provide a thorough explanation of this*

I basically lined the holes up on the Kreg cabinet hardware jig to 3 inches. I had a 3″ cabinet pull. I place the cabinet hardware onto the particle board. I latched and tightened the Kreg clamp onto the hardware jig and particle board to hold in place.

Example of holding the hardware jig up with the Kreg clamp.

From there, I took my drill using the 3/16 drill bit and drilled a hole in the hole part on the cabinet hardware jig (gray hole area). Then I screwed the screws into the board and tighten with my drill using my Ryobi driving set.

Example of drilling the hole through the hardware jig on the cabinet.

For my kitchen, I’ve decided to use acrylic cabinet pulls from Amazon. For the top cabinets and draws, I’ll use the 5″ center ones. For the lower cabinets, I’ll use the acrylic cabinet knobs.

P.S. I like ordering from Amazon because you can get a pack of 10,15, etc and spend next to nothing. The acrylic ones tend to be $5 each no matter where you go. If you’re going for a different look, try my Amazon store for cabinet pull ideas and grab a pack.