According to a Merrill Lynch survey, over 80% of the people in this country believe that homeownership is still “an important part of the American Dream”. There are many financial and non-financial reasons people feel this way.

One of the biggest reasons is because it helps build family wealth. Last week, Freddie Mac posted about the power of home equity. They explained:

“In the simplest terms, equity is the difference between how much your home is worth and how much you owe on your mortgage. You build equity by paying down your mortgage over time and through your home’s appreciation. In a nutshell, your money is working for you and contributing toward your financial future.”

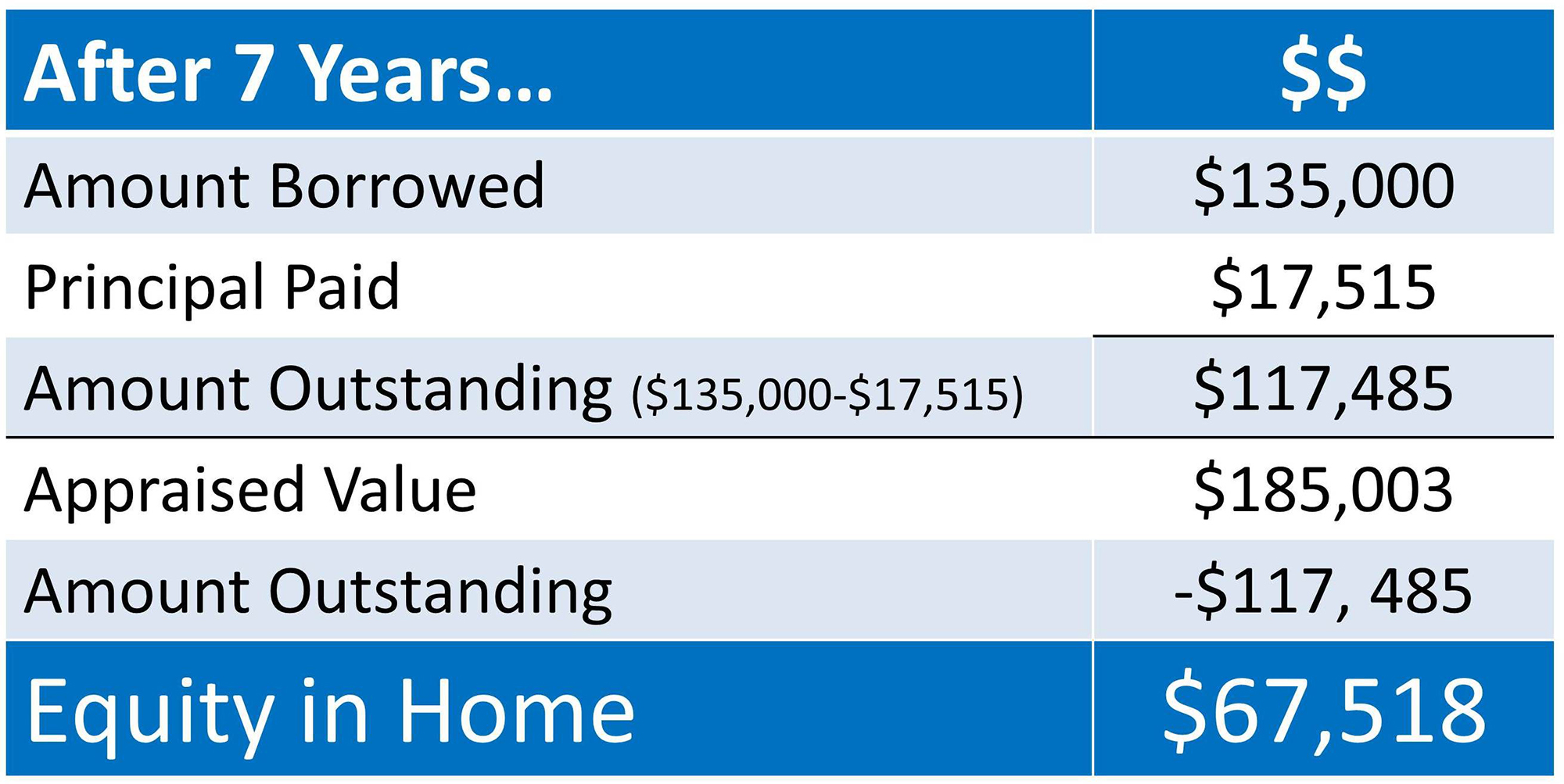

They went on to show an example where a person bought a home for $150,000 with a down payment of 10%, resulting in a loan amount of $135,000. The buyer secured a 30-year fixed-rate mortgage at 4.5% with a monthly mortgage payment of $684.03 (not including taxes and insurance). They then illustrated what would happen after seven years of making a mortgage payment, assuming 3% per year home appreciation (the historic national average):

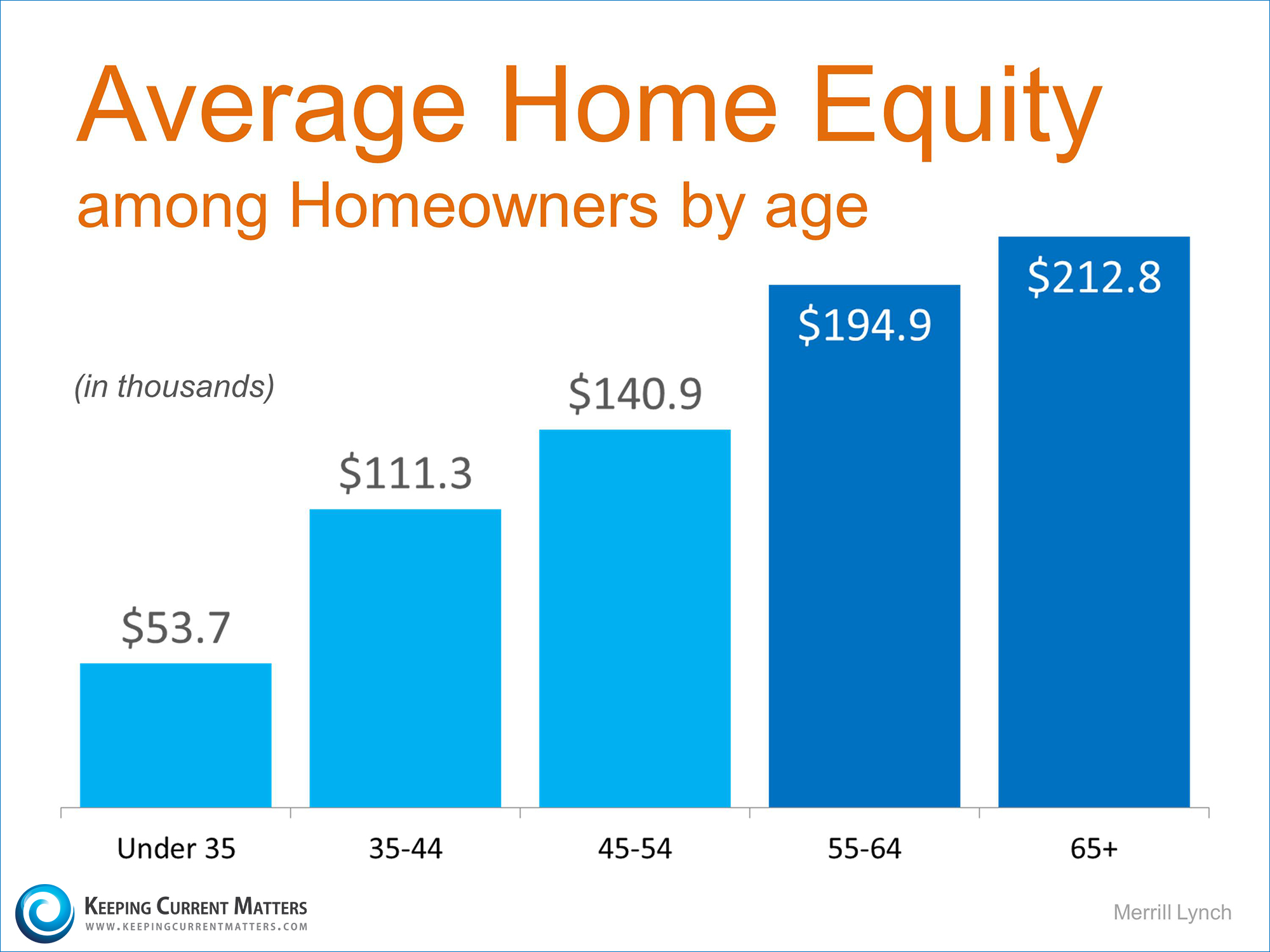

And that number continues to build as you continue to own the home. Merrill Lynchpublished a report earlier this year that showed the average equity homeowners have acquired at certain ages.

Bottom Line

Home equity is important to building wealth as a family. Referring to the first scenario above, Freddie Mac explained:

“Now, if you continued to rent, and made the same payment of $684.03 per month, you’d have zero equity and no means to build it.Building equity is a critical part of homeownership and can help you create financial stability.”