One of the biggest challenges for potential homeowners is their credit score. I work as a part time Housing Counselor at a local nonprofit helping low to moderate income families become homeowners. A question that I am frequently asked is “what credit score do I need to purchase a home?” The answer would be whatever the lender thinks is beneficial. I say this because each lender is different and have their own underwriting criteria. I personally know lenders that will qualify you for a mortgage at 580, 620, or 640 by the least. Of course the higher the score, the lower the interest rate but as low as rates are today, you can still can a favorable rate at 580.

In order to rebuild your credit you will need the following things: a spending plan and your credit report. Notice how I did not say budget. In my counseling sessions budgeting is a forbidden word. It seems like someone is restricting you and makes you feel as if you don’t live. Let’s break away from the conservative word of budgeting and instead let’s develop a spending plan. A spending plan breaks down where you spend your money each month. Now in order to rebuild or build your credit you will have to know where you are financially. With your spending plan, you want to distinguish your housing expenses, debt expenses, savings, and any “play” money. Once you designate a place to put your money, then you will have a spending plan. Every dollar needs to a have place in order to determine a spending plan.

After you realize where you are financially, you want to see if you have any savings. Savings is going to be a key on whether you can pay down debt (if you have any). I recommend that before you pay anyone, you pay yourself. You should try to take at least 10% of your net income (the amount of your paycheck that you take home) and put it in your savings. I know you’re thinking, “Andrea, 10% is a lot for me to take out from each paycheck when I barely make any money.” If 10% is too much, lower to 5% or a dollar amount that you makes you comfortable. The key to this is develop a habit. Lenders like a habit like this. I say 10% because look at it like the example below:

Net Income: $2000

10% Savings: $200

Savings for a year: $2400

See how you could easily save thousands in one year with the 10% gesture. That doesn’t seem as bad when it is put like that huh? You can even suggest your payroll deduct your 10% so that you don’t see it anyway.

Credit Report

This may be another topic all by itself but for this blog post I wanted to make it short and simple. To be honest, in order to rebuild your credit, it is short and simple. Let’s start with some basic guidelines.

1. You are allowed one free credit report a year. Click this link to receive your credit report from the three major credit bureaus: Annual Credit Report. I’ve been faithfully doing this since I was a freshman in college. There was a seminar that was given about checking your credit report. I don’t recall if they talked about credit because this is all I remembered from the seminar. Please keep in mind that I was 17 and a freshman at LSU. I had partying and football games on my brain (nevermind that this was the summer either…I was fresh off the sand’s of mama’s given curfew)

2. If you have collectors calling you now, answer. When you don’t answer, you are only diffusing the problem. Some collectors can and will sue you for unpaid debt but you must know your state’s statute of limitations. We will discuss this later (just by stating this I know the credit report will be another post).Tell them your situation and see what options the may have for you. ONLY commit to a payment plan with a collector if the collection is still with the original creditor. If not, ask them to cease phone calls and to contact you through mail only. You will always want things in writing. This is the proof you will need for any disputes.

3. I always get potential housing counseling clients or real estate clients saying that my credit score is this and when the lender pulls it is lower than originally expected. This is because the free scores that you find online are built on a Vantage score. In easier terms, the big boys (TransUnion, Equifax, and Experian) decided they didn’t want to pay FICO the big bucks for numbers so they created their own scoring system.Mortgage lenders look for your FICO score. Credit scoring varies based on who the lender is. Mortgage lenders have different scoring than car lenders. So the score given to you at the car lot is probably much different than what is given for a mortgage. For mortgage purposes, you will need your FICO score.

Now to the meat of the report. Most people are concerned with the credit score. As of right now, if you are focused on a score, please STOP. I repeat STOP. When you are rebuilding your credit, the score does not matter. You’re probably thinking “Andrea, you just told me that I need a certain score to get my house.” My answer to that is you do need a certain score but when you are rebuilding your credit it isn’t your score that is important but what’s in your credit report. Your credit report determines your score. Once you start working on rebuilding your credit, your score will rise. It is kind of like the saying, “if you build, they will come.” Remember that in your course of working on your credit. “If you build your credit, that 700 or 800 will come.”

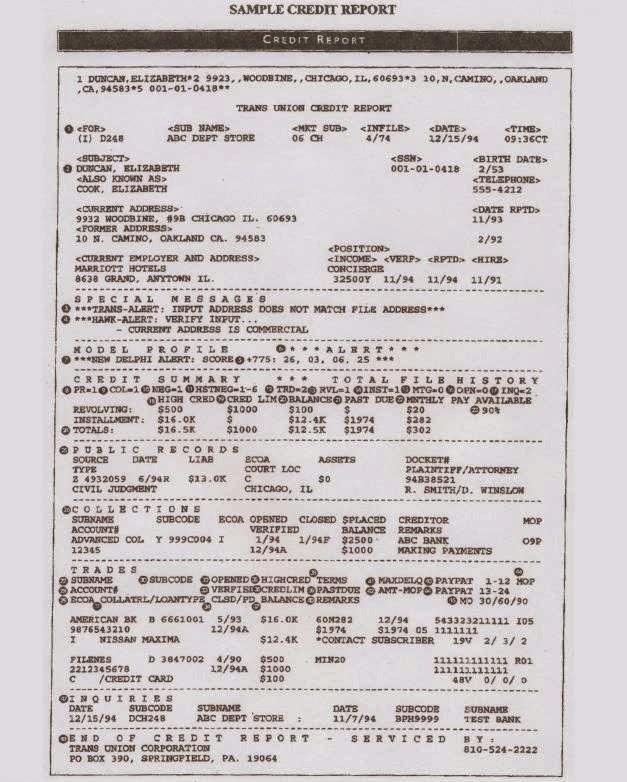

A sample credit report looks similar to this: